Impact of UAE’s 64% Surge in Trademark Registrations: What Businesses Should Know

The UAE’s trademark landscape is no longer defined by a short-term registration jump. It now reflects the sustained maturation of the IP ecosystem, supported by the UAE’s position as the 30th-ranked economy in the Global Innovation Index 2025. By the end of September 2025, the UAE had reached 402,311 registered national and international trademarks, turning the registry into a more crowded and competitive arena. Lets delve into why businesses are waking up to the need for a registered trademark to protect their brands in this fast-moving market.

The Strategic Imperative of Intellectual Property in 2026

In 2026, trademark protection is directly linked to the UAE’s wider “We the UAE 2031” vision, which aims to build a more innovation-led and knowledge-based economy. For businesses, this means IP is no longer just legal paperwork. It is a commercial asset, a market-entry safeguard, and a growth tool.

The 64% Surge in Numbers

Numbers do not lie. The earlier Q1 2024 rise has now developed into a stronger 2025 trend. In the first half of 2025, the Ministry of Economy and Tourism registered 19,957 national and international trademarks, a 129% increase compared with 8,711 trademarks in H1 2024. What if your brand is left unprotected while others get ahead? Many are now trying out tools like free trademark search in UAE to make sure their assets stay safe and strong in a competitive landscape.

Why it Matters for Businesses

This is not just numbers. It shows growing trust in UAE’s business world and investors feeling confident. But in 2026, the bigger issue is crowding. With more than 400,000 trademarks already registered, businesses need to act earlier, check similarity more carefully, and secure brand rights before competitors file first. Getting a registered trademark early can really boost credibility, set your brand apart, and give you a solid footing in an innovation-driven market.

UAE as Global Business Hub

UAE has become a real hotspot for trade, innovation, and investment. With digitized processes and solid legal protection, companies feel safer to expand. This also supports the UAE’s 2031 ambition to become a global hub for the new economy. What if your business misses this wave? Lets delve into how UAE’s smart IP frameworks and forward-thinking rules help startups, SMEs, and investors protect their brands efficiently.

Understanding Trademark Registration in the UAE

Ever wondered why a registered trademark matters so much for businesses in UAE? Well, imagine building a brand and someone else using your name or logo. That can be a nightmare. Lets delve into how trademarks protect your identity, give you legal rights, and ensure your business stands out in a market as competitive as Dubai and Abu Dhabi.

What is a Trademark

A trademark is basically your business signature. It could be a name, logo, slogan, or even a symbol. In 2026, businesses are also paying more attention to non-traditional marks, including 3D shapes, holograms, sounds, product packaging, and other distinctive signs that can separate one brand from another. How is that important? It sets you apart and stops others from copying your identity. Every smart business in UAE knows securing a registered trademark is more than paperwork. It is a shield that keeps your brand safe.

Types of Trademarks in 2026

| Type | What it protects |

| Word mark | Business names, product names, and brand names |

| Logo mark | Visual identity, icons, symbols, and stylized marks |

| Slogan mark | Taglines and short brand phrases |

| 3D mark | Product shapes, packaging, and distinctive physical appearance |

| Sound mark | Recognizable audio linked to a brand |

| Hologram mark | Distinctive holographic or visual effects used as brand identifiers |

| Geographical Indication | Local agricultural, natural, or artisanal products linked to a specific UAE region or origin |

UAE Trademark Registration Process

The UAE trademark registration process starts with checking whether the mark is available and whether it conflicts with an existing registered mark. First, you search your mark using free trademark search in UAE tools. Then submit applications online, pay fees, and wait for approval. Lets delve into why many prefer trademark registration agents in Dubai to avoid mistakes and speed up the process. It saves time and reduces rejection risks. Learn more about our Trademark Registration Service for step-by-step guidance.

The UAE remains largely a first-to-file jurisdiction. This means prior use of a brand is usually not enough if another party has already secured a registered mark. Filing early is therefore safer than relying on market use alone.

Legal Frameworks Supporting Trademarks

UAE follows global standards like the Paris Convention and TRIPS Agreement. This ensures your trademark is recognized internationally. What if you are a foreign investor? Knowing these frameworks gives confidence that your IP rights are enforceable. Businesses also leverage legal due diligence consultancy

to review mark availability, classification accuracy, and possible conflicts before filing. Check our Legal Due Diligence Consultancy for guidance.

In May 2025, the UAE also introduced a federal Geographical Indications system to protect national products with qualities, reputation, or characteristics linked to specific UAE regions. This gives local producers stronger protection against misuse of regional names and helps promote UAE-origin products in local and global markets.

Role of UAE Ministry of Economy

The Ministry of Economy is key to registration and protection. Digitized systems speed up approval. Civil and criminal enforcement gives businesses confidence. In 2026, the Ministry’s role has expanded further through new trademark service fees, the One Day TM Initiative, Geographical Indications, AI-supported IP services, and stronger digital trademark infrastructure. How is that your company can feel secure while others rush to register? Lets delve into how these protections make UAE a safe and attractive place for startups, SMEs, and big investors alike.

Analysis of the 64% Surge: What Drove the Increase?

The earlier 64% rise has now been overtaken by a stronger H1 2025 trend. The UAE recorded 19,957 national and international trademark registrations in the first half of 2025, compared with 8,711 in H1 2024, marking 129% growth. Lets delve into the sectors driving this surge. From smart technology to transportation, F&B, pharmaceuticals, medical devices, finance, and real estate, businesses now realize the value of a registered trademark in Dubai and Abu Dhabi.

Technology and Sustainability: The 2026 Filing Hotspots

In 2026, smart technology and pharmaceuticals remain strong filing areas, but green technology and AI-driven services are becoming major growth drivers. The UAE’s Green Intellectual Property roadmap, launched in February 2025, has pushed sustainability, circular economy, clean technology, and innovation-led projects deeper into the IP conversation.

Sector-wise Surge

Smart technology and transportation lead the way, closely followed by F&B, pharma, medical devices, finance, and real estate. Green technology and AI-driven services are now joining this list as businesses move to protect names, platforms, product lines, and digital service identities before the market becomes more crowded. What if your business is in one of these sectors? Lots of businesses now try trademark registration offer services to lock in their IP fast. A registered trademark gives them real protection in a competitive market.

Investor Confidence and IP Awareness

The spike shows growing trust in UAE’s IP laws. Businesses realize protecting brands is essential. How is that investors feel safe while startups expand? Lets delve into why awareness of intellectual property rights is spreading fast. Companies now see IP as a real business asset worth investing in and safeguarding properly. This is especially important for AI, software, health-tech, and sustainability businesses, where brand ownership often supports funding, licensing, and expansion discussions.

Digitized Registration Services

The Ministry of Economy made registration simple. Online applications, faster approvals, and digitized systems help companies act quickly. Some even use free trademark search in UAE to avoid conflicts. In 2026, this search step matters even more because a larger registry increases the risk of similar marks, objections, and classification errors. Check out our Trademark Registration Service to see how tech speeds up approvals and protects brands across UAE, including Dubai and Abu Dhabi.

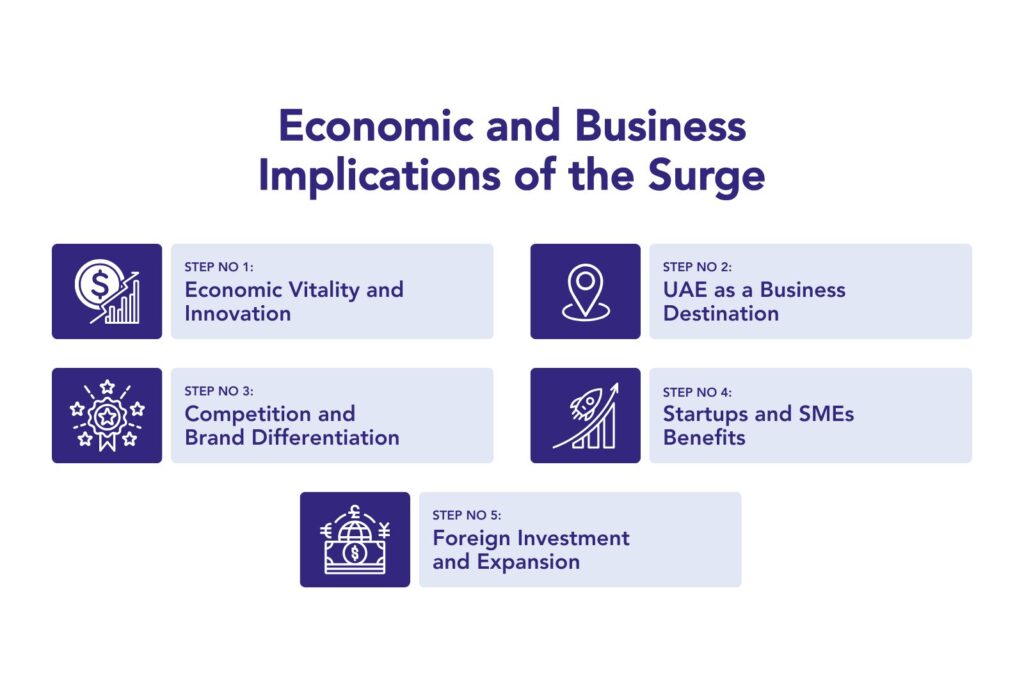

Economic and Business Implications of the Surge

UAE’s trademark growth is now about more than registration volume. In 2026, trademarks are becoming business assets that can be protected, valued, transferred, assigned, and used to support expansion. Companies in Dubai and Abu Dhabi see IP as asset. How do you protect ideas while staying ahead? Well, a registered trademark gives that edge, sparks creativity, and helps businesses grow in fast-moving markets.

Economic Vitality and Innovation

Trademark growth signals lively economy. Companies invest in new products knowing IP is safe. What if your business waits? Early action with a trademark registration offer can be more affordable for eligible businesses, as National SME Programme members now receive a 50% reduction on trademark service fees, while People of Determination receive a full exemption. Innovation plus protection equals long-term growth and stronger positioning. Some businesses even feel more confident launching ideas across Dubai and Abu Dhabi now.

Intangible Assets as Collateral: The TM Market Place

The UAE has also introduced the TM Marketplace, a government-supported digital platform that allows businesses to list, buy, sell, or assign registered trademarks. This gives startups and investors another route: instead of building every brand from scratch, they may acquire an existing mark or use assignment as a practical alternative where filing conflicts arise.

UAE as a Business Destination

UAE is drawing global firms like never before. Investors trust legal protections and easy systems. Just imagine your brand thriving here. Think about it: a registered trademark makes UAE a safe choice for expansion and cross-border partnerships. Companies now see IP protection as a serious part of business planning. The TM Market Place also strengthens this appeal by making trademarks more visible as tradeable commercial assets.

Competition and Brand Differentiation

A registered trademark builds identity and loyalty. How do you stand out in crowded markets? Many now see trademarks as strategic tools. They help win customers, protect reputation, and command respect. In Dubai or Abu Dhabi, having your brand legally secured gives real credibility beyond just marketing or social campaigns. In a registry with more than 400,000 marks, differentiation now has to be tested before launch, not after the brand is already public.

Startups and SMEs Benefits

Startups and SMEs benefit big. Trademarks safeguard unique ideas and brand stories. What if competitor copies concept? Many now leverage trademark registration agents in Dubai to secure IP efficiently. Early registration gives peace of mind. Lets face it, protecting brand lets small businesses focus on growth, innovation, and making their mark in UAE. The 50% SME fee reduction also makes early filing less expensive for eligible National SME Programme members.

Foreign Investment and Expansion

Foreign investors love UAE’s IP-friendly market. Safe trademarks encourage cross-border business and partnerships. How do you attract international collaborators? Well, protecting a registered trademark makes expansion easier and investment safer. Companies see value beyond borders, in Dubai, Abu Dhabi, and other emirates. IP is now part of serious growth strategy. UAE brands are also becoming more outward-looking, with stronger use of international filing routes such as the Madrid Protocol and overseas trademark systems.

Legal Protections and Enforcement of Trademarks in UAE

You might ask, how secure are brands here. In 2026, the answer is clearer: the UAE has moved from basic protection to active enforcement. Civil and criminal tools are available. Businesses often worry what if copies hit shelves. In Abu Dhabi alone, counterfeit and non-compliant goods worth more than AED 1.8 million were seized in 2025, supported by 16,748 ADRA inspection visits. In this part, you will see why enforcement in the UAE is both feared and respected.

Civil Remedies and Market Protection

A registered trademark gives owners a stronger basis to seek civil remedies once their mark is copied. Courts may grant damages or order injunctions. In some cases counterfeit goods are seized right away. How is that for quick response. The law works like shield. Sometimes it feels like sword too, giving genuine businesses clear upper hand.

Criminal Penalties and Counterfeit Control

In the UAE, counterfeiting is more than a business risk. It is crime. Commercial-scale infringement can attract fines of up to AED 1,000,000, along with possible imprisonment, seizure, and destruction of counterfeit goods. Fake goods are destroyed to warn others. Through initiatives such as Project Zero, authorities are also exploring more sustainable ways to deal with seized counterfeit products instead of treating enforcement as a simple disposal exercise. Some people ask, is this too harsh. But the truth is, such action keeps the market clean and helps honest players grow stronger.

Online and Digital Enforcement: Protecting Brands in the E-commerce Era

Brand misuse is no longer limited to physical shelves. In 2026, UAE businesses also need to monitor online marketplaces, social media pages, look-alike packaging, fake seller accounts, and unauthorized logo use. Digital enforcement has become part of trademark protection, especially for consumer brands, technology platforms, and cross-border sellers.

Building Confidence for Businesses

Awareness of these protections changes how businesses operate. They know investment in brand identity is safe. Customers get more trust in what they buy. Without such law, fake goods would take over. But here, competition stays fair. Loyalty is built on real products, not on clever copies flooding the market.

Steps Businesses Should Take in Light of the Surge

So what should companies do now that trademarks in the UAE are surging. Some rush late, others get copied fast. Better approach is simple. Start early. Treat brand protection as foundation, not afterthought. In 2026, that also means reviewing existing portfolios against the Nice 13th Edition and planning filings through a 30/90/180-day trademark audit cycle. In this part, you will see why early registering trademarks is a must and how experts help.

Register Early and Cover Completely

Smart firms move quick. They secure registering trademarks before the idea spreads. Scope matters too. Cover logos, names, slogans together. That way loopholes are avoided. Many ask, what if I expand later. Well, without wide cover, space for growth shrinks. For urgent launches, the UAE’s One-Day Trademark Examination service, available for AED 2,250, can help businesses obtain faster initial examination feedback. Early steps may feel costly but save far more later.

Keep Watch and Defend the Mark

Getting a certificate is one thing. Monitoring and protecting trademarks is another. Brands should track misuse online, in shops, even in ads. Some fakes slip in quietly. Guess what, once ignored they multiply. Quick response stops bigger loss. Law in the UAE is strict, but owners must stay alert too. This is where periodic portfolio reviews, marketplace checks, and customs or enforcement readiness become practical safeguards.

2026 Trademark Compliance Audit

| Timeline | What to check |

| 30 days | Run trademark searches, check similar marks, and review priority brand names. |

| 90 days | Review Nice 13th Edition classifications, filing documents, and Power of Attorney status. |

| 180 days | Monitor use, renewal dates, enforcement gaps, and marks that may face non-use risk. |

Trademarks as Growth Drivers

Some think a mark is just legal formality. Not true. A registered mark is a business asset. It builds loyalty, attracts partners, and helps in funding. Imagine two startups. One with a strong brand. Another with none. Investors trust the first. Why. Because protection signals stability, and stability fuels growth.

Get the Right Guidance

The process can feel tricky. Here trademark attorneys and trademark consultants make it smoother. They know classes, documents, appeals. Their role saves time and costly errors. Administrative Decision No. 2 of 2026 also gives applicants more flexibility by allowing monthly 30-day extensions for submitting the Power of Attorney, provided the extension is requested before the current deadline expires. For official steps, businesses can check the UAE Ministry of Economy trademark guide. With experts and the right info, the path becomes far less complex.

Challenges and Considerations Amid Increased Registrations

Now comes the flip side. With the rise in filings, not all paths are smooth. Some sectors feel crowded. Others deal with copycats. This part explores issues like mark similarity, enforcement complexities, and why trademark searches with proper due diligence save trouble. Let us see where risks hide and how to handle them.

Crowding and Similar Marks

Popular industries attract most applications. That leads to mark similarity headaches. With more than 400,000 trademarks already registered in the UAE, even small similarities in names, logos, or sounds can create filing objections or disputes. Two logos may look alike, or names may sound close. When that happens, disputes rise. The law helps, but the process drags. Careful planning and unique branding save time. Simple rule, stand out early, and competitors cannot trap you later.

Value of Careful Checks

Many rush in without checks. But skipping trademark searches and ignoring due diligence is risky. In 2026, businesses should treat legal due diligence consultancy as part of the filing strategy, especially where AI-powered search tools, logo similarity checks, and Nice 13 classification reviews are needed. Imagine months of work only to face rejection. That burns money and energy. A smart business first investigates what exists. They make sure the ground is clear. It feels slow at first, yet prevents bigger setbacks later.

Speed Versus Accuracy

Everyone wants quick filings. The speed of registration does matter. The 24-hour examination option helps time-sensitive launches, but speed should not replace proper clearance checks. However, racing too fast may create errors. Wrong classes or vague coverage mean weak protection. On the other side, endless delays invite imitators. The trick is balance. File fast, but check twice. Accuracy makes the mark solid, and speed keeps rivals away.

When Rules Get Complex

Even after success, enforcement complexities can show up. A company may win registration but struggle to stop infringers. Why. Because cross-border cases, online sales, and fake goods complicate matters. There is also a non-use cancellation risk: if a mark sits unused for five consecutive years, third parties may challenge it. The solution lies in vigilance and legal support. Rights are powerful, but only if owners are active in guarding them every day.

Future Outlook: What to Expect for UAE Businesses

So what lies ahead. UAE businesses must gear up for bigger changes. More IP registrations, stronger legal reforms, and smart technological upgrades are shaping the market. Add to that an expanding role in global IP frameworks. This shift also supports the “We the UAE 2031” vision of building a more knowledge-based and innovation-led economy. The stage is set. The question is. How can firms stay sharp in this fast game.

Rising Curve Ahead

The numbers are not slowing. In fact, IP registrations keep climbing. Just in nine months, growth hit thirty nine percent. That signals trust and ambition. What if this continues. Companies will face even tighter competition. Staying ahead will need not just ideas but also smart protection strategies that secure brands early and well.

Shifts in Law

The government is pushing legal reforms to keep pace with innovation. Rules are getting clearer, penalties are stricter, and processes are smoother. In 2025, the UAE also moved toward AI-driven legislative frameworks, where technology can help review, update, and improve laws faster. That builds confidence for investors. It also warns infringers that the risk is high. For firms, the smart move is to study changes closely and use them as shields for growth.

Tech Driven Systems

Technological upgrades are turning IP services faster and more user friendly. Online filing, AI powered checks, and digital monitoring make protection easier. Blockchain may also become more useful for recording IP transactions, licensing history, ownership changes, and brand assignments in a more secure and traceable way. This saves both time and cost. Businesses can file, track, and defend marks from anywhere. If you want to explore current tools, visit the UAE Ministry of Economy’s portal.

The Role of AI and Blockchain in UAE IP Protection

AI can help businesses search similar marks, monitor online misuse, and prepare cleaner filings. Blockchain can support stronger records for ownership, licensing, and assignments. Together, these tools may make trademark protection faster, more transparent, and harder to manipulate.

Global Ties

The UAE is not working alone. Through global IP frameworks, its role is expanding. That means local marks gain wider reach abroad. It also helps foreign firms trust the UAE as a safe market. For local entrepreneurs, this is a doorway. Protecting a mark here may soon open smoother entry into global ventures. Brands also need to think about Answer Engine Optimization, because AI tools now influence how customers discover and compare businesses online.

How ADEPTS Supports Businesses in Navigating Trademark Registration

So, how do UAE businesses actually turn laws into gains. That is where ADEPTS steps in. With proven IP strategy and sharp trademark registration skills, the firm makes complex rules look simple. The goal is clear. Build confidence. Guard ideas. And set brands on a track that makes growth secure and lasting.

Expert Edge

ADEPTS brings expertise that covers all aspects of IP strategy. From market scans to filing advice, the firm helps cut risks and boost returns. This includes portfolio auditing for Nice 13 compliance, classification review, and expedited filing representation where timing is critical. Their approach is not one-size-fits-all. Each client gets guidance shaped around sector needs. What does that mean. It means fewer mistakes, faster moves, and more control over brand future.

Tailored for UAE

Every market has its own rules. ADEPTS understands UAE businesses better. Services are tailored to match local laws while keeping global reach in mind. That balance matters. Protecting a brand in Dubai or Abu Dhabi is one thing. Making sure it is respected abroad is another. ADEPTS helps strike both with ease.

Best Practices in Play

Strong intellectual property management is not just about filing papers. It is about running systems that keep marks safe long term. ADEPTS trains teams, sets checks, and uses tools to monitor risks. It also helps businesses assess renewal deadlines, non-use risk, online infringement, and whether expedited examination is worth using. This keeps firms ready against threats. Want to see how their services unfold. Visit ADEPTS Trademark Consultancy to learn more.

Partnership Advantage

In the end, support is about trust. ADEPTS partners with firms not just as consultants but as long-term guides. The focus is on securing brand strength and building a durable edge in crowded markets. With expert trademark registration and strategy, businesses get a shield and a sword. For businesses looking for trademark registration agents in dubai, ADEPTS helps connect legal process, filing strategy, and practical brand protection in one advisory approach. That is a deal worth taking.

FAQs:

Usually, UAE trademark registration takes four to seven months under the standard route. The UAE also offers an expedited one-day examination option for AED 2,250, although publication, opposition, and final registration steps still follow the normal process. Sounds fast, right? But delays pop up if papers are missing or if someone objects. Still, compared to other countries, the UAE moves quick. Best trick is filing early. That way UAE businesses stay ahead and do not risk someone else jumping first.

They can, but not directly on their own. Foreign firms need a local agent or consultant to file. The law makes it that way to keep things smooth. Many overseas companies see trademark registration in the UAE as their first serious step into Gulf markets. It is like buying a ticket to entry. Look for Jafza Free Zone here.

Costs include official fees, lawyer charges, and sometimes translations. For a standard UAE trademark filing, the official fee is typically AED 6,500 per class, including AED 750 application fee, AED 750 publication fee, and AED 5,000 final registration fee. At first, it feels pricey, but the protection lasts years. Think of it as insurance. Skipping it can be way more expensive later. For a breakdown, check this UAE Trademark Registration Cost Resource. Many UAE businesses use it before planning budgets.

A trademark registration here lasts ten years. After that, it needs renewal. Miss the deadline and rights can slip away fast. On top of that, brands must keep an eye out for trademark infringement. Many UAE businesses hire consultants just to monitor the market. Better to pay a little now than fight later.

Simple truth. No trademark registration, no strong protection. Anyone can copy your brand, and fighting back is messy. Courts rely on registered marks, not just use. That means higher costs, loss of customers, even damage to reputation. For UAE businesses, skipping it is like leaving your shop door open all night.

Good news. One UAE trademark covers all seven emirates. No need to file separately for Dubai, Abu Dhabi, or the rest. Saves money and time. But remember, if you want global reach, you must file abroad or use treaties. Local protection is just the first solid step toward bigger markets.

Not really. A UAE trademark only protects inside the country. To go global, companies use the Madrid Protocol or file in each country. Still, a UAE filing shows you mean business. Many UAE businesses first secure home ground. Then they use it as leverage when stepping onto the world stage.

Disputes go through courts or official channels. Judges can block sales, award damages, or even order fake goods seized. In tough cases, criminal penalties apply. The system is strict, and trademark infringement does not get ignored. UAE businesses who act fast usually save money and brand trust. Waiting too long often hurts.

Administrative Decision No. 2 of 2026 gives trademark applicants more flexibility with Power of Attorney submissions. Instead of facing automatic rejection after the initial deadline, applicants may request monthly extensions, provided the request is made before the current period expires. This is especially useful for foreign applicants dealing with notarisation, legalisation, and translation delays.

References

- BLOCKCHAIN ADOPTION IN THE GULF STATES.

https://mei.edu/wp-content/uploads/2019/12/Blockchain-in-the-Gulf.pdf. - ‘Coming on January 1, 2026: Thirteenth Edition of the Nice Classification’. Madrid-System,

https://www.wipo.int/en/web/madrid-system/w/news/2025/coming-on-january-1-2026-thirteenth-edition-of-the-nice-classification. - Dubai Customs Dubai Customs – Smart Trade and Border Services.

https://www.dubaicustoms.gov.ae/en/Pages/default.aspx. - Federal Decree by Law Concerning Promulgating the Commercial Transactions Law.

https://uaelegislation.gov.ae/en/legislations/1610. - ‘Https://Www.Wipo.Int/Gii-Ranking/En’. GII 2025 Innovation Ecosystems & Data Explorer,

https://www.wipo.int/gii-ranking/en. - ‘Ministry of Economy and Tourism Introduces Trademark Service Fees as Part of Efforts to Enhance UAE’s Appeal for National and International Brands and Support SME Owners’. Ministry of Economy and Tourism UAE,

https://www.moet.gov.ae/-/ministry-of-economy-and-tourism-introduces-trademark-service-fees-as-part-of-efforts-to-enhance-uae-s-appeal-for-national-and-international-brands-and-support-sme-owners. - ‘Ministry of Economy and Tourism Launches Trademark Platform “TM Market Place”’. Ministry of Economy and Tourism UAE,

https://www.moet.gov.ae/-/ministry-of-economy-and-tourism-launches-trademark-platform-tm-market-place-. - ‘Ministry of Economy and Tourism Organizes “Reinforcing Intangibles to Strengthen the Economy” Conference to Stimulate Investment in R&D and Innovative Projects’. Ministry of Economy and Tourism UAE, https://www.moet.gov.ae/-/ministry-of-economy-and-tourism-organizes-reinforcing-intangibles-to-strengthen-the-economy-conference-to-stimulate-investment-in-r-d-and-innovative-projects.

- ‘Nice Classification’. Classification-Nice, https://www.wipo.int/en/web/classification-nice

- ‘Register Trademark’. Ministry of Economy and Tourism UAE,

https://www.moet.gov.ae/ar/w/%D9%82%D9%8A%D8%AF-%D8%B9%D9%84%D8%A7%D9%85%D8%A9-%D8%AA%D8%AC%D8%A7%D8%B1%D9%8A%D8%A9 - UAE Vision 2031 Strategic Intelligence. https://intelligence.wetheuae.ae/home.

- Value of Counterfeit Goods Seized Tops AED1.8 Million in 2025: ADRA.

https://www.wam.ae/en/article/176kz9i-value-counterfeit-goods-seized-tops-aed18-million. - Young, Ernst &. Abu Dhabi Registration Authority | ADRA. https://www.adra.gov.ae/en/.