Financial Management for Small Businesses in UAE: 2026 Strategies for Growth & Compliance

Small businesses mean small funds, but this definitely does not have to mean small growth. Running and growing a small business all comes down to meticulously managing money. In the UAE’s maturing regulatory environment, business owners now operate in a landscape where 2026 marks the conclusion of the first full corporate tax cycles and the shift toward active enforcement rather than education.

With a fast-changing market and compliance-driven oversight, business owners need innovative financial strategies to keep things running smoothly. The UAE’s AED 92.4 billion Federal Budget for 2026 further reinforces government-led growth opportunities for compliant and well-structured small businesses.

By incorporating simple steps in their business such as tracking down every expense, planning and budgeting, and paying off all debts timely can make a big difference. Utilizing the right tools efficiently and staying up to date with evolving regulatory requirements under the 2026 compliance framework can help businesses stay profitable.

In this article, we’ll break down easy and practical UAE small business financial management 2026 tips to help small businesses succeed, so keep reading to learn more!

Why Financial Management is Critical for UAE SMEs in 2026

A penny saved is a penny earned. Financial management is not just for the SMEs but also for big businesses. In 2026, financial management has shifted from preparing for tax compliance to surviving and operating confidently in the enforcement phase of UAE taxation. In order to grow your business, you need to budget and plan every penny that you spend, while ensuring your financial records, controls, and reporting can withstand regulatory scrutiny.

Taxation is one of the most critical yet often overlooked aspects of running a business. Paying more than necessary can significantly reduce your profit margins and limit opportunities for growth.

On the other hand, underpaying—even unintentionally—can lead to audits, fines, and reputational damage. In a more competitive 2026 market, strategic financial planning is now essential not only for compliance but also to build credibility with banks, lenders, and potential investors. Striking the right balance is essential to maintaining financial health, staying compliant, and positioning your business for long-term success in an economy projected to grow by 5.3% in 2026.

Therefore, understanding UAE Small Business Financial Management 2026 is very important for all businesses operating in the UAE’s high-growth environment, where SMEs with formal business plans are shown to outperform their peers by approximately 20%.

UAE’s 2026 Regulatory Landscape

The UAE government has set out a maturing and enforcement-driven regulatory framework effective from January 1, 2026, under Federal Decree-Laws No. 16 and 17 of 2025, that businesses must now operate within.

These rules focus on taxes and financial reporting, so SMEs need to understand Corporate Tax compliance for UAE SMEs in a post-learning, enforcement-focused environment to avoid penalties and ensure smooth business operations.

The updated laws significantly expand the Federal Tax Authority’s audit powers, including extended record-keeping expectations and audit look-back periods of up to 15 years in cases of tax evasion, along with stricter timelines for record updates and corrections.

Corporate Tax Expansion

The focus in 2026 has moved away from introductory tax rates toward mandatory registration and filing deadlines. While the 0% corporate tax rate continues to apply to taxable income of AED 375,000 or less, and a 9% corporate tax applies on income exceeding this threshold, the critical compliance risk now lies in meeting statutory filing timelines rather than understanding rates.

For Juridical Persons (companies), the first UAE Corporate Tax return must be filed by September 30, 2026, under the “9-month rule.” Missing this deadline triggers penalties and a 14% annual interest rate on unpaid corporate tax.

Natural Persons (including freelancers and sole proprietors) are also brought squarely into scope in 2026. If their 2025 business turnover exceeded AED 1 million, they must register for Corporate Tax by March 31, 2026.

Key 2026 Corporate Tax Deadlines

| Taxpayer Type | Key Requirement | Deadline |

| Juridical Persons (Companies) | Corporate Tax Return Filing | September 30, 2026 |

| Natural Persons (Freelancers / Individuals) | Corporate Tax Registration (if 2025 turnover > AED 1 million) | March 31, 2026 |

Additionally, free zone entities remain subject to economic substance and activity reporting, with greater scrutiny in 2026 to demonstrate real operational presence rather than form-only structures.

VAT and Excise Tax Updates

Value Added Tax (VAT) is a tax on goods and services that businesses collect from customers and pay to the government. It affects the product/service’s prices, the company’s profits, and production costs, so SMEs must manage it carefully, particularly by using VAT automation tools Dubai to maintain accuracy and timely compliance. In the UAE, businesses must register for VAT if their taxable supplies and imports exceed AED 375,000 annually. Voluntary registration is allowed if the taxable turnover or expenses exceed AED 187,500. Staying informed about these thresholds helps ensure compliance and supports sound financial planning.

Additionally, the UAE government has introduced taxes on single-use plastics to encourage businesses to choose eco-friendly alternatives and help protect the environment.

The 5-Year Expiry Rule

As of 2026, VAT credits are no longer subject to indefinite carry-forward. Under Federal Decree-Law No. 16 of 2025, VAT credits originating from 2021 will begin expiring if they are not claimed within the prescribed five-year period. This makes periodic VAT reviews, reconciliations, and the use of VAT automation tools Dubai essential to avoid permanent loss of recoverable VAT.

Tiered Sugar Tax

Effective January 1, 2026, the UAE has replaced the previous 50% flat excise tax on sweetened drinks with a tiered excise tax model based on sugar content. Under this system, beverages with higher sugar levels attract higher excise rates, for example, approximately AED 1.09 per liter for high-sugar drinks. This change directly impacts pricing, margins, and excise compliance for affected SMEs.

Economic Challenges in 2026

Regardless of the relaxation provided by the UAE government, running a business is going to come with a lot of challenges.

In 2026, these challenges are less about global inflation, which is projected to remain low at approximately 1.8% and more about strategic agility, operational efficiency, and digital readiness. With the ongoing shift toward a cashless and digitally enabled economy, running a business is now harder for SMEs that fail to adapt their systems, payment methods, and internal controls to remain competitive.

Apart from this, while geopolitical issues in nearby regions continue to influence supply chains, the primary pressure for UAE businesses in 2026 comes from maintaining margins in a stable but highly competitive and mature market. Businesses are increasingly required to operate with higher efficiency, faster decision-making, and stronger financial discipline to remain profitable.

Core Financial Management Strategies for 2026

Budgeting is not a one-size-fits-all approach; it highly depends on the size of the business, its expenses, and financial goals.

Budgeting and Forecasting

Here are a few UAE small business financial management 2026 ways that can assist small businesses to budget intelligently. Regardless of the relaxation provided by the UAE government, running a business is going to come with a lot of challenges. In 2026, the focus of budgeting and forecasting has shifted toward automation, accuracy, and real-time decision-making rather than manual projections.

Zero-Based Budgeting for SMEs

Zero based budgeting is when the firm sets a new budget every year. Instead of adjusting and carrying forward last year’s costs and expenses, the management sits down together and evaluate every expense and cost that is predicted to be incurred that year.

This helps the business justify every penny that is predicted to be spent and allows them to cut down on unnecessary expenses while utilizing the saved money for more important things, like marketing or customer service.

Did you know, a Dubai-based F&B startup used the zero-based budgeting technique in the year 2024 as part of its preparation for a stricter 2026 compliance and cost-efficiency environment.

The startup analyzed its expenses and eliminated unnecessary costs. They refined their supplier contracts and reallocated resources, which resulted in costs being reduced by 30% and it gave them sufficient funds to reinvest their savings into marketing and customer experience.

AI-Powered Forecasting Tools

Another method that has been proven successful when it comes to budgeting and forecasting is the use of appropriate AI powered forecasting tools. These tools provide accurate results to the businesses when it comes to making predictions about the cash flow. Apart from this, the tools also help in keeping a check on expenses, and planning for future growth by automatically generating forecasts and explaining variances rather than relying on manual inputs.

They analyze the trends and provide real-time insights that help the small businesses make informed decisions. In 2026, traditional tools are increasingly being replaced by agent-based FP&A platforms such as Prophix One, ChatFin AI, and Datarails FP&A Genius, which can automatically complete budgets, flag anomalies, and support faster decision-making, rather than earlier-generation tools like flocast.ae and Zoho Finance Suite that primarily focused on automation and tracking.

Managing Cash Flow in High-Cost Environments

Cash flow management means making sure a business has enough money coming in to cover its expenses. In a high-cost environment (where rent, salaries, and other expenses are high), businesses need to be extra careful about how they handle their cash.

Tactics to Improve Liquidity

Liquidity refers to the situation where the business has access to money in the form of cash. Businesses can sell their unpaid invoices to platforms like Beehive.ae to get instant cash instead of waiting for customers to pay. Another way to improve liquidity is by asking suppliers for longer payment terms can help businesses hold onto cash for a longer time, improving financial stability.

Avoiding Cash Flow Pitfalls

Apart from selling your invoices and asking suppliers for longer payment terms, one thing that small businesses must be doing is to avoid any cash pitfalls. A cashflow pitfall is referred to a situation where the businesses suffer lack of liquid cash flow. This can either be because a business relies too much on post dated checks or trusts its customers too much and they take too long to pay.

These situations are pitfalls as they lead the businesses to cash shortages and avoiding over reliance on post dated cheques and providing customers with long debts can ensure that a business does not suffer cash flow problems especially if they want to survive in a high cost environment.

Dubai’s Cashless Strategy 2026

As part of Dubai’s Cashless Strategy 2026, businesses are increasingly expected to move toward digital transactions by default. Shifting away from cash and post-dated cheques to digital payments improves real-time cash flow visibility, reduces reconciliation time, and minimizes manual errors. For SMEs, adopting digital payment systems supports faster collections, clearer audit trails, and more accurate cash flow monitoring, which is critical in a cost-sensitive operating environment.

Debt Management

The third strategy when it comes to managing finances in a small business is to manage your debt smartly. Yes, when running a small business there are a lot of challenges that a business may face and if the budgeting and financing is not done accurately, chances are that the business will fall in debt sooner or later.

To keep your business healthy and make smart decisions about borrowing money and repaying loans, you must know exactly when to get a loan and how you can leverage the UAE Central Bank’s 2026 loan.

When to get a loan?

Businesses should take loans when they need funds for growth, expansion, or managing short-term cash flow gaps, but only if they can afford to repay. In 2026, the UAE offers SME loan programs like the Emirates NBD Business Quick Loan, which provides faster access to funds for small businesses.

Refinancing High-Interest Debt

If a business has expensive loans with high interest rates, refinancing means replacing them with new loans at lower rates to reduce monthly payments. In 2026, the UAE Central Bank’s interest rate cuts will allow businesses to refinance and save money on repayments.

Navigating UAE Tax Compliance in 2026

Understanding taxes is tedious and can get nerve recking quickly, but staying compliant is important to avoid penalties. Here’s what small businesses in the UAE need to know for 2026, as compliance has moved firmly into the enforcement phase rather than education.

Corporate Tax Registration and Filing

The first and the most important thing for all businesses to do, no matter the size of the company, is to register for corporate tax and file their returns on time. In fact, the UAE government introduced EmaraTax Portal to make this process easier. In 2026, timely registration, accurate filing, and record updates are closely monitored by the Federal Tax Authority (FTA).

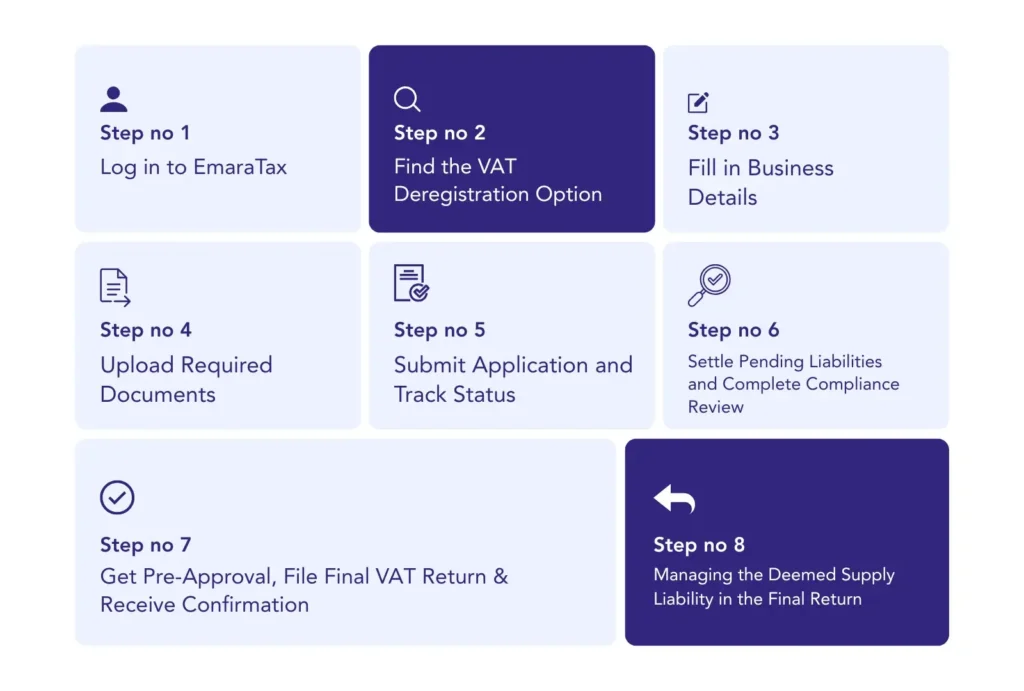

Step-by-Step Guide to EmaraTax Portal

- Log in to the EmaraTax Portal using your business credentials, or create an account if you’re a new user.

- Complete your Corporate Tax registration if it is still pending, to ensure you are eligible to file and pay taxes.

- Navigate to the relevant Corporate Tax section on the dashboard to begin the filing process.

- Complete your business profile by entering all required information and uploading the necessary documents.

- The system will assist in calculating your corporate tax liability based on the income you declare.

- Review all entered details carefully and submit your corporate tax return before the deadline.

- Pay the calculated tax amount using the available payment options within the portal.

- Once payment is made, you will receive an official confirmation from the Federal Tax Authority (FTA) acknowledging receipt.

- Businesses must also notify the FTA of any changes to their records—such as trade license details, ownership, or activities—within 20 business days to avoid administrative penalties.

Small Business Relief (SBR) 2026 Updates

Did you know that if your revenue is less than AED 3 million, you can apply for Small Business Relief (SBR) and get an exemption from corporate tax.? Small Business Relief (SBR) remains available only for tax periods ending on or before December 31, 2026, after which eligibility and relief conditions may change.

However, you must officially apply for it through the EmaraTax Portal so your business can stay on track and avoid any issues in the future.

VAT Best Practices

Staying on top of VAT is not easy, but with the right tools and a little smartness, it doesn’t have to be hard. Here are some simple ways to make VAT compliance easier in 2026, as procedural requirements continue to evolve.

Automating VAT Returns

If you’re manually filling your VAT returns, that is a risky business, and this can cause mistakes to creep in and cost you unnecessary fines. Using tools like TallyPrime UAE Edition and FTA’s VAT Compliance Dashboard, this software helps you generate VAT invoices and file returns without breaking a sweat while tracking your VAT obligations and ensuring you don’t miss deadlines.

From January 1, 2026, self-invoicing under the Reverse Charge Mechanism (RCM) is no longer required, reducing administrative effort but increasing the importance of maintaining proper standard documentation to support reverse charge transactions.

Common VAT Mistakes to Avoid

Many businesses tend to make mistakes when it comes to VAT. Here are some common mistakes that you need to be aware of:

- Some things are VAT-exempted, this means you cannot claim back the tax and therefore you must double-check before filing to avoid any trouble.

- Forgetting to pay VAT means penalties for late VAT filing in UAE 2026. Under the new penalty framework, late payments are now subject to a 14% annual interest rate, charged monthly, replacing the previous 2% immediate and 4% monthly penalty structure.

- The FTA requires businesses to keep records for at least five years. If they ever ask for them and you don’t have them, you could face penalties of AED 10,000 per violation, which will apply for the first offense, with repeat violations incurring fines of AED 20,000 if committed within 24 months.

- Under the updated tax procedures, failure to maintain or update records within prescribed timelines can result in stricter enforcement actions.

Leveraging Technology for Financial Efficiency

Living in the 21st century and not using technology means you are missing out on efficiency and convenience in your business.

Top 2026 Accounting Software for UAE SMEs

Here are the Best cloud accounting software for UAE startups:

Cloud-Based Solutions

Cloud-based solutions are amazing tools that allow you to store terabytes of data online. These tools allow you to manage your business finances without needing any physical paperwork or software installed on a computer.

Cloud-based tools like QuickBooks Online, Xero with FTA integration are amazing cloud-based tools that are conveniently available at economical prices and very easy to use, allowing you to manage finances efficiently and enabling you to access your accounts from anywhere and avoid the headache of paperwork piling up.

Blockchain for Transparency

The Dubai Blockchain Platform is amongst the Best cloud accounting software for UAE startups. It ensures financial records are super secure and can’t be changed or tampered with. This technology helps businesses keep their transactions transparent and trustworthy.

Blockchain-based tools like this are great for SMEs looking to build trust with investors, auditors, and even customers. They make accounting easier, reduce errors, and allow businesses to focus on growth without worrying about financial fraud or record manipulation.

AI-Driven Financial Advisors

Did you know that there are AI-driven tools that can actually give you some very valuable advice on managing your finances?

Smart tools like Wealthface and SIRON AML are amazing when it comes to AI-driven financial advisors. While Wealthface guides you on where you can invest your extra income by creating personalized investment plans based on your financial goals, the SIRON AML detects fraud and suspicious activities so you can stay away from unnecessary problems.

These advisory tools allow you to make informed decisions and stay on the right side of the law, without having to spend hours in your office.

Electronic Invoicing System (EIS) Roadmap

As part of the UAE’s transition toward a fully digital tax and compliance ecosystem, the Electronic Invoicing System (EIS) roadmap introduces machine-readable XML/JSON invoices that will gradually replace traditional PDF invoices.

A pilot phase is scheduled to commence on July 1, 2026, initially targeting larger businesses. Under this roadmap, large firms will be required to appoint an Accredited Service Provider (ASP) by July 31, 2026, to ensure system connectivity and compliance.

Although SMEs are not immediately mandated, 2026 is the recommended transition year for small businesses to begin aligning their accounting systems and Best cloud accounting software for UAE startups with EIS-ready capabilities, reducing future compliance risk and manual rework.

Funding and Grants for UAE SMEs in 2026

UAE government cares for it’s people especially those who are contributing to the economy positively, therefore, it has introduced funding programs for the startups that assists them when it comes to incorporating technology and promote eco-friendly practices, in 2026, the focus of government support has shifted from pure cash grants to market access, scalability, and integration into federal supply chains.

Government-Backed Programs

Here is what the government backed programs are that offer funding and grants to startups:

Khalifa Fund’s 2026 Expansion

The khalifa fund initiatives now include the “SME Champions” platform, which connects eligible SMEs directly with government and semi-government procurement opportunities valued at over AED 672 million, moving beyond one-time funding toward long-term revenue access. The program is offering up to AED 2 million just to make sure that the businesses do not face any financial stress and can grow with a stronger emphasis on readiness for government contracts rather than upfront financial aid.

If you are wondering how to apply through the Khalifa Fund SME Champions platform, just head to the Khalifa Fund portal, submit your business profile, and demonstrate operational capability, compliance readiness, and alignment with government procurement requirements.

Mohammed Bin Rashid Innovation Fund

This is also a funding program that has been started by the UAE government called Mohammed Bin Rashid Innovation Fund, under the MBRIF 11th Cohort (2026), the program continues to support innovation-led SMEs, with funding structures increasingly linked to commercialization, partnerships, and market deployment rather than standalone financing. This specific program provides small startups with access to guarantees and financing support, particularly for AI, advanced technology, and green energy projects, while facilitating connections to strategic partners and government-backed initiatives.

Alternative Financing

Not every small business owner is comfortable with the idea of taking loans as they fear losing control of the business. Here are two alternative financing methods that businesses can use to generate finance:

Crowdfunding

In the crowdfunding method, you do not go to the bank asking for loans; instead, you approach other people who want to invest in your company. There are further divisions in crowdfunding:

- Eureeca

Eureeca is an alternative financing method for equity funding. This is where people invest money in your business, and in return, they get a small share of your company. - Liwwa

Liwwa connects businesses with individual lenders through peer-to-peer lending. Instead of going to a bank, you borrow money from regular people who want to invest. You pay them back with interest, just like a bank loan.

Venture Debt

Some businesses grow really fast and need money but don’t want to sell shares. Venture debt is a type of loan that helps these businesses get funding without giving up ownership. Companies like Shorooq Partners help businesses get these special loans so they can keep growing while still staying in control.

Avoiding Costly Financial Mistakes

Case Study: A Dubai SMEs Costly Penalty

A Dubai-based SME learned the lesson of avoiding costly financial mistakes the hard way when they mixed personal and business accounts. This oversight resulted in a hefty AED 50,000 Economic Substance Regulation (ESR) non-compliance fine , a costly lesson in financial management.

Top 5 Compliance Mistakes to Avoid

To protect your business from unnecessary penalties, be mindful of these common financial missteps under the 2026 penalty framework introduced through Cabinet Decision No. 129:

- Missing Corporate Tax or VAT filing deadlines – While the 2026 penalty reform replaces daily compounding fines, late tax payments now attract a 14% annual interest rate, making delays expensive over time despite the simplified structure.

- Submitting incorrect tax returns – First-time incorrect returns are now subject to a reduced fixed penalty of AED 500, but repeated errors or material misstatements can still trigger audits and stricter enforcement actions.

- Underreporting income – Attempting to reduce corporate tax liability can lead to reassessments, penalties, and prolonged audits, with enforcement in 2026 focused heavily on accuracy of declared income.

- Ignoring payroll and Emiratisation compliance – Failing to meet Emiratisation quotas or maintain proper payroll records can attract penalties and disrupt business operations, particularly as cross-agency data matching increases.

- Poor record maintenance – Inadequate or outdated records can result in penalties and interest exposure, especially with stricter filing duties and extended audit review powers under the current enforcement regime.

Future-Proofing Your Finances: 2026 Trends

The financial landscape is evolving fast, and staying prepared is key! From sustainability-focused loans to digital payment innovations, here’s what SMEs need to watch out for as they prepare beyond 2026 and into 2027.

ESG-Linked Financing

Sustainability is no longer just an ethical choice, it’s a financial advantage. Banks like Mashreq are now offering lower interest rates for SMEs that adopt environmentally and socially responsible practices. This trend presents a unique opportunity for businesses to secure cost-effective financing while enhancing their ESG (Environmental, Social, and Governance) credentials.

Central Bank Digital Currency (CBDC)

The UAE’s Digital Dirham pilot program is set to revolutionize cross-border payments. As part of Digital Dirham Phase 2, the focus has expanded to wholesale and retail cross-border use cases, enabling businesses to benefit from faster settlements, lower transaction costs, and improved payment transparency, a game-changer for SMEs engaged in international trade.

FAQs:

In most cases, older errors are better disclosed earlier. Depending on timing, waiting until April 2026 may result in higher cumulative penalties compared to the current fixed penalty regime.

The repetition rule applies only if the same violation occurs within 24 months. After that period, the breach is generally treated as a first-time offence again.

No. While self-invoicing is removed, businesses must still retain the supplier invoice and proof of payment to support any VAT position taken.

A system failure refers to technical issues that prevent issuing or transmitting e-invoices in the required format, particularly prolonged ERP or ASP outages.

In most cases, natural persons are subject to the AED 1 million turnover rule rather than Free Zone qualifying income rules. If the AED 1 million threshold was exceeded during 2025, Corporate Tax registration must be completed by March 31, 2026.

The date of supply is generally determined by the digital wallet confirmation, which serves as the legally relevant transaction timestamp.

Refunds may be available for eligible overpayments, including certain administrative penalties, provided claims are submitted within the allowed timeframe.

Yes. Participation in digital payment platforms does not remove tax transparency or reporting obligations where they otherwise apply.

The threshold is generally calculated exclusive of VAT. Where the threshold was exceeded in 2025, registration is required by March 31, 2026.

The ASP must support multi-entity access, data segregation, and consolidated reporting under the group TRN.

No. Once the deadline lapses, the right to claim or offset those credits is lost.

The new interest-based model replaces the previous compounding penalty structure for post-April 2026 violations.

Yes. A registered Legal Representative remains mandatory, and failures to notify the FTA may attract penalties.

Accepting crypto as payment alone does not usually make an SME a VASP. Additional services such as custody or exchange would change this position.

Core funding and AI Mentor programs are generally reserved for Emirati entrepreneurs, though non-Emiratis may benefit indirectly through partnerships.

An administrative penalty of AED 500 per month applies, together with 14% annual interest on any unpaid tax.

References

- Business Funding in UAE | Enterprise and Startup Fund’. Khalifa Fund, https://www.khalifafund.ae/.

- Croedfunding UAE.

https://u.ae/en/information-and-services/business/public-private-people-partnership/pppp/crowdfunding. - ‘Financial Crime Compliance Software | Siron®One’. IMTF,

https://imtf.com/siron-one-financial-crime-compliance-software/. - ‘Mohammed Bin Rashid Innovation Fund & Accelerator | MBRIF’. Mohammed Bin Rashid Innovation Fund,

https://mbrif.ae/. - Radware Captcha Page.

- Small Business Relief.

https://tax.gov.ae/DataFolder/Files/Guides/CT/Small%20Business%20Relief%20Guide%20-%20EN%20-%2027%2008%202023.pdf. - ‘Wealthface: Grow Your Wealth | Invest, Trade, Save and Factor Investing.’ Wealthface,

https://wealthface.com/. - Federal Budget Framework- UAE Ministry of Finance,

https://mof.gov.ae/federal-budget-framework-and-process/. - EmaraTaxPortal, https://u.ae/en/information-and-services/finance-and-investment/taxation/emaratax .

- Central Bank Digital Currency Strategy – the Digital Dirham,

https://u.ae/en/about-the-uae/strategies-initiatives-and-awards/strategies-plans-and-visions/finance-and-economy/central-bank-digital-currency-strategy. - Abdou, Mahmoud. ‘Maktoum Bin Mohammed: The Federal Budget for the Fiscal Year 2026 Represents a Milestone in the Journey of Government Work’. Ministry of Finance – United Arab Emirates, 27 Oct. 2025,

https://mof.gov.ae/en/news/maktoum-bin-mohammed-the-federal-budget-for-the-fiscal-year-2026-represents-a-milestone-in-the-journey-of-government-work/. - ———. ‘Ministry of Finance Announces Cabinet Resolution on Implementing Reverse Charge Mechanism for VAT on Scrap-Metal Trading’. Ministry of Finance – United Arab Emirates, 19 Dec. 2025,

https://mof.gov.ae/en/news/ministry-of-finance-announces-cabinet-resolution-on-implementing-reverse-charge-mechanism-for-vat-on-scrap-metal-trading/. - ‘eInvoicing’. Ministry of Finance – United Arab Emirates,

https://mof.gov.ae/en/about-ministry/mof-initiatives/einvoicing/. - Federal Tax Authority – Corporate Tax Topics.

https://tax.gov.ae/en/taxes/corporate.tax/corporate.tax.topics/resident.juridical.person.aspx. - List and Contact Details of the Ministry of Finance Pre-Approved eInvoicing Service Providers.

https://mof.gov.ae/wp-content/uploads/2025/10/Pre-approved-service-providers-page.pdf. - MBRIF Welcomes 11th Cohort of Innovators into Innovation Accelerator Programme.

https://www.wam.ae/en/article/byb1xf3-mbrif-welcomes-11th-cohort-innovators-into. - ‘New Excise Tax from January 1: UAE Classifies Four Categories of Sweetened Products’. Khaleej Times,

https://www.khaleejtimes.com/uae/new-excise-tax-january-1-2026-four-categories-sweetened-products. - Taxation of Natural Persons under the Corporate Tax Law Corporate Tax Guide | CTGTNP1.

https://tax.gov.ae/Datafolder/Files/Guides/CT/Taxation%20of%20natural%20persons%20-%2025%2011%202023.pdf. - The Authority’s Policy on Issuing Clarifications and Directives.

https://tax.gov.ae/Datafolder/Files/Legislation/FTA-Decision-No-2-of-2025.pdf. - ‘UAE Economic Expansion Set to Scale New Highs in 2026’. Khaleej Times,

https://www.khaleejtimes.com/business/economy/uae-economic-expansion-set-to-scale-new-highs-in-2026.