Corporate Tax for Freelancers and Sole Proprietors in the UAE: 2026 Compliance Checklist

The UAE’s corporate tax regime came into effect on June 1, 2023. Since then, businesses of all sizes have had to adjust. It happens every time corporate tax changes. Freelancers and sole proprietors are no exception either.

Freelancers and proprietors are part of the economy just like everyone else. Many people still think corporate tax is only for large companies. It’s not. If you earn business income in your own name, you may fall under its scope. And this is why, in 2025, you need to keep an eye on compliance with the latest corporate tax. It is no longer optional and non compliance will have repercussions.

Freelancers and solo entrepreneurs need to know what applies and what doesn’t. They should be on the right side of the law. That’s where ADEPTS comes in. We help freelancers and sole proprietors understand the rules, prepare the right records, and file returns without stress. So you can focus on your work, while we handle the numbers.

Understanding Corporate Tax in the UAE for Freelancers and Sole Proprietors

Who exactly qualifies as a freelancer or sole proprietor under the UAE’s corporate tax law? If you work for yourself, you are one. you’re considered a natural person conducting a business activity. You may be a designer, consultant, developer, writer, or any other independent professional, anything. If you offer services in your own name it means you need to understand how the corporate tax regime applies to you.

One common misunderstanding is that corporate tax only affects big companies. In reality, natural persons who carry on business activities must register and pay tax if their income crosses the required thresholds.

The first point to know is the annual turnover requirement: if your total business income for the year is more than AED 1 million, you are required to register for corporate tax. Remember, turnover means your total business earnings before expenses. So if you have multiple clients or larger projects, it’s easier to reach this limit than many freelancers realise.

CRITICAL WARNING FOR 2026: If your business turnover exceeded AED 1 Million in 2025, you MUST register for Corporate Tax by March 31, 2026. Missing this deadline results in an automatic AED 10,000 fine. This penalty applies even if you were unaware of the requirement.

Important clarification for the 2026 “1 Million” Turnover Test: This threshold is based on gross revenue (total money received before expenses). You must exclude personal salary from employment, residential rental income, and personal investment returns. Only business activity income counts toward the AED 1 Million turnover threshold.

Once registered, you won’t pay tax on your entire income. The UAE has set a tax-free threshold of AED 375,000 on taxable profits, which means you only pay tax on the amount that exceeds this. For example, if your freelance income for the year is AED 1.5 million and your net profit after allowable expenses is AED 500,000, you will pay tax on AED 125,000 which is the amount above the AED 375,000 threshold at the standard rate of 9%.

It also helps to know the difference between working as you and working through a company. If you’re freelancing or running a small gig in your own name, you’re what the law calls a natural person. In this case, your freelance income is taxed under your personal name, and you stick to the thresholds we just talked about.

But things change if you’ve set up an LLC, a Free Zone company, or any other legal structure. Now, you’re running a juridical person — basically, your business is its own separate entity in the eyes of the tax authorities. This means it has its own tax registration, its own books, and sometimes its own deadlines and obligations.

So, take a step back and look at how you’re set up. Are you working as yourself, or does your business have its own legal name and license? This one detail decides which rules you follow. Missing it could cost you time, money, or even penalties down the line.

A lot of freelancers feel corporate tax is complicated and stressful. But it doesn’t have to be. It really comes down to three things: know if you qualify, check your turnover and profit numbers, and keep your records clear. Once you have that sorted, you’ll find that staying compliant isn’t a headache. It just gives you freedom to do your thing without worrying about anything.

Registration Requirements and Deadlines for 2026

If your freelance income crosses AED 1 million in a year, registering for corporate tax with the Federal Tax Authority (FTA) isn’t optional anymore. It is now mandatory. Many freelancers miss this point because they think “I work alone, so tax rules for big businesses don’t apply.” But the moment your revenue hits that threshold, you’re expected to get registered.

For 2026, if your 2025 turnover crossed AED 1 Million, your registration deadline is March 31, 2026. Missing this deadline triggers an automatic AED 10,000 late registration penalty.

Registration must be completed through the FTA’s EmaraTax portal. A Golden Visa or Freelance Permit does NOT automatically register you for Corporate Tax. You must obtain a specific Corporate Tax Registration Number (TRN) to be compliant.

The deadline matters too. If your business income in 2024 crosses the limit, you must complete your registration by March 31, 2025. Missing the deadline can be costly. The FTA can impose penalties ranging from AED 10,000 to AED 20,000, just for late registration or not registering at all. That’s money better spent on your business, not on fines.

This is exactly where ADEPTS can take the pressure off your shoulders. We handle the paperwork, review your numbers, and make sure your registration is done right and on time. So you don’t have to worry about penalities in tax return UAE.

Corporate Tax Filing Process for Freelancers and Sole Proprietors

Once you’re registered, filing your tax return each year is the next big step. Many freelancers put this off until the last minute, but with the right plan, it doesn’t have to be a scramble.

Here’s how it works:

1. Get Your Tax Registration Number (TRN):

Once you’re registered with the FTA, you’ll receive your TRN. This is your official ID for all things corporate tax so keep it safe and handy.

2. Prepare Your Financial Statements:

Gather your invoices, bank statements, expense records, and any other documents that show your business income and costs. Good record-keeping is key here. If your numbers aren’t clear, you risk errors or delays when you file.

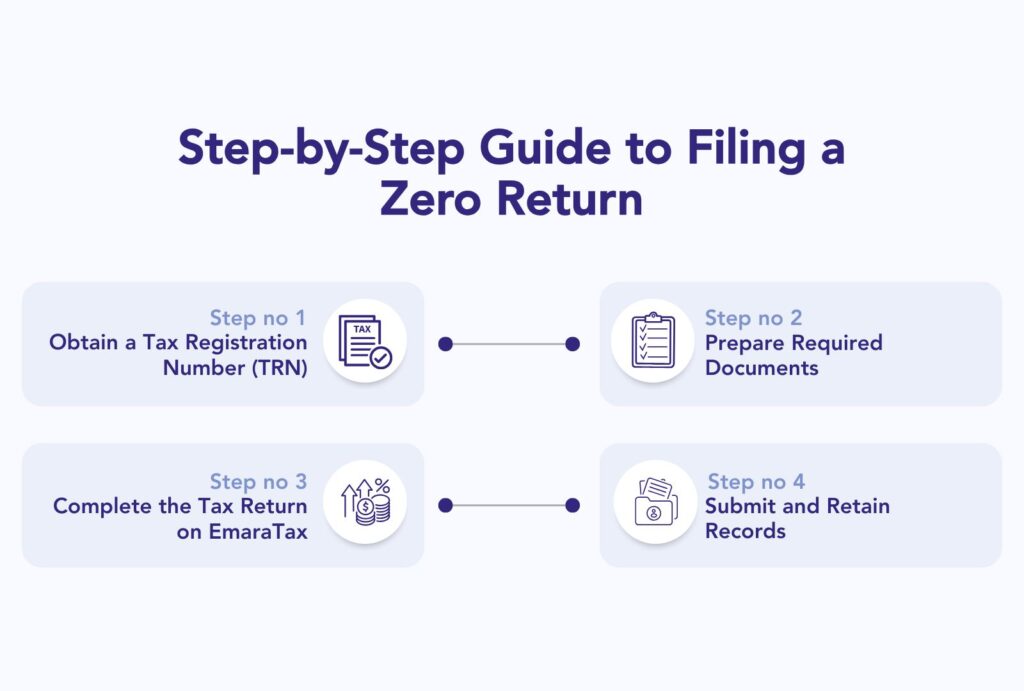

3. File Through EmaraTax:

The UAE uses the EmaraTax platform for corporate tax filing. It is so easy to go through the whole process via eservices FTA. Just log in, follow the steps, fill out your details, and upload your financial information.

4. Know Your Filing Deadline:

You have up to 9 months after your financial year ends to file your return. For example, if you follow the calendar year, your filing deadline for 2025 income will be September 30, 2026. For the 2025 tax period, the filing deadline will generally fall on September 30, 2026 (for calendar-year freelancers). Even if you qualify for 0% tax under Small Business Relief, you must still file your return by this deadline.

5. Watch for Common Pitfalls:

Late filing, incomplete documents, or inaccurate profit calculations can all get you in trouble. A small mistake today can become a big headache tomorrow. If you plan to close your freelance license, you must deregister for Corporate Tax within 3 months of license cancellation. Failure to deregister can lead to additional administrative penalties.

That’s why so many freelancers rely on ADEPTS. We make sure your books are clean, your numbers add up, and your returns go in on time. You can get on with serving your clients while we handle the forms.

Calculating Taxable Income: What Freelancers Need to Know

You think UAE income tax is due on all your income? Taxable income isn’t the same as what hits your bank account. You only pay tax on your net profit, not your total revenue. That means you’re allowed to subtract your business expenses before calculating how much tax you owe.

If you’re spending on tools, software, rent, internet, marketing, or anything directly tied to your work, those are likely deductible. But personal spending doesn’t count, and neither does any salary you “pay yourself” if you’re working as a sole proprietor. That’s not considered a business expense.

Accuracy matters here. Keep proper records. Every receipt, invoice, and statement tells the story of your business—and that story needs to be clear if you’re ever audited or asked to explain your numbers.

Starting April 14, 2026, under the new Unified Penalty Regime, the FTA is significantly increasing its focus on documentation readiness. Freelancers must retain all invoices, bank statements, contracts, and expense receipts for a minimum of 7 years. Failure to provide records during an audit can result in penalties ranging from AED 10,000 to AED 20,000.

If your revenue is over AED 1 million but under AED 3 million, there’s something called the Small Business Relief Program. It can reduce your corporate tax burden or even remove it entirely for a limited period. But it’s not automatic—you have to meet the criteria and file accordingly.

URGENT 2026 UPDATE: Small Business Relief (SBR) is currently only available for tax periods ending on or before December 31, 2026. Freelancers with revenue below AED 3 Million can elect for 0% tax, but this relief must be explicitly selected in the tax return. It is not applied automatically. This may be the last chance to benefit from SBR under current rules.

Also, if you have income coming in from multiple places—say, social media, consulting, sponsored content, or online courses—it all adds up. Don’t assume each stream gets treated separately. If it’s part of your business activity, it’s all part of the same tax calculation. Make things easy by calculating it all via FTA eservice.

Revenue earned from international platforms like Upwork, Fiverr, Amazon, or other global marketplaces counts toward the AED 1 Million turnover threshold if the activity is conducted as part of your UAE business.

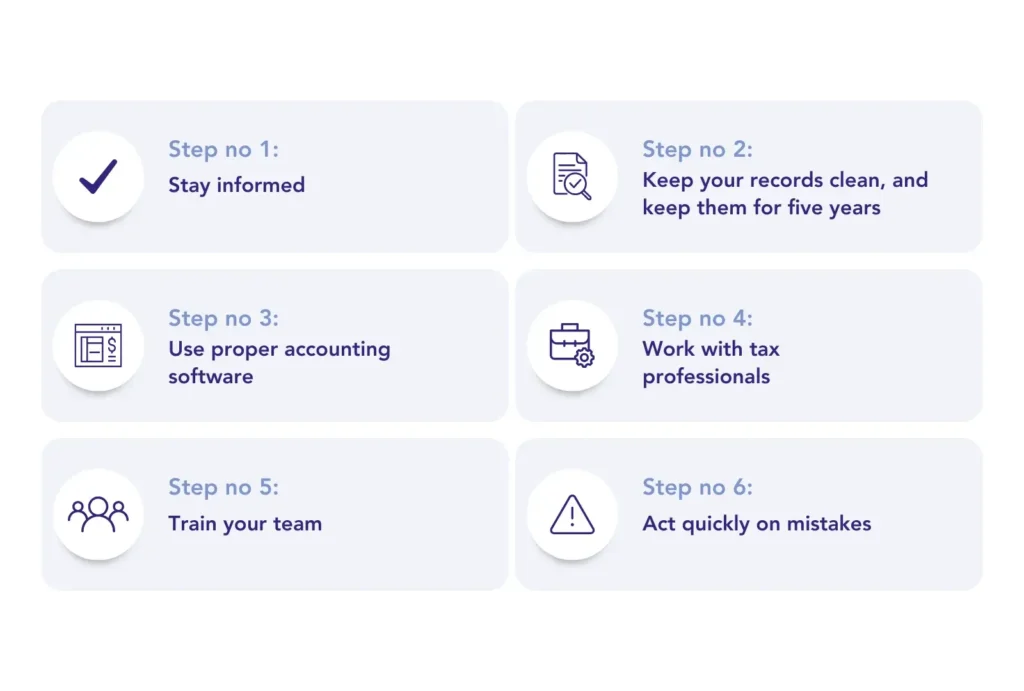

Compliance Best Practices for 2026

Stay organized. Don’t wait for the year to end to look at your numbers.

Doing a monthly or quarterly review keeps things manageable and helps you spot issues early. You don’t need to become an accountant—but you do need to know what’s going on with your income, expenses, and profit.

With new and stern laws in place, bookkeeping is a must. You should not be ignoring it. No matter what you are doing, keep a record. With simple records, you may be able to do it alone. With more complex settings, you will need professionals’ help.

In 2026, documentation readiness is not optional. Surprise audit requests are increasing, and failure to maintain digital records for 7 years can trigger significant administrative penalties.

That’s where firms like ADEPTS can make a real difference. We take care of the technical side so you can focus on your clients and your work.

Finally, tax rules aren’t static. UAE regulations are still evolving. What’s true this year might change next year. Make it a habit to check for updates or ask someone who tracks this full-time.

Consequences of Non-Compliance

- Missed deadlines, poor records, or skipped registration can result in real penalties. Not small ones either—fines can go up to AED 20,000 or more, depending on the issue.

- Specifically, missing the March 31, 2026 registration deadline after crossing the AED 1 Million threshold in 2025 results in an automatic AED 10,000 fine.

- Non-compliance can put your trade license at risk. And if you rely on a license to bill clients, that’s your whole business on the line.

- Reputation matters too. A tax issue on your record can make it harder to work with agencies, corporate clients, or international partners. Many now ask for proof of tax registration and clean compliance.

How ADEPTS Supports Freelancers and Sole Proprietors in UAE Tax Compliance

Tax rules are changing fast. So are the ways people work. If you’re freelancing or running a one-person business, you need more than generic advice. You need answers that fit how you actually work.

That’s what ADEPTS does best. We don’t just tick boxes. We offer tax advisory that makes sense for your industry, your income streams, your income tax return filing and your personal goals.

We help you get registered properly with the Federal Tax Authority so you don’t miss deadlines. We keep your books in order so your numbers hold up if the FTA ever comes knocking. And we make sure your returns go in on time, with every allowable expense claimed and every relief you’re entitled to.

But the real value is the peace of mind. You know exactly where you stand, you know what’s coming up, and you’re not left guessing what penalty might land in your inbox.

Conclusion

Corporate tax is here to stay. It’s no longer just a conversation for big companies or people with teams and office towers. Freelancers and solo business owners are in the picture now too.

Understanding how the rules apply to you isn’t just good practice — it’s your responsibility. But you don’t have to do it alone. Start early. Get advice that’s grounded in the UAE’s actual tax law, not guesswork. And if you want to make sure nothing slips through the cracks, let ADEPTS handle the heavy lifting for you.

Ready to make compliance simple? Reach out to ADEPTS today and take control of your tax situation before it takes control of you.

FAQs:

Yes. Corporate tax applies based on your business activity and turnover — not just your trade license status. If you are conducting a business in your own name and your turnover exceeds AED 1 Million, you may still be required to register and comply.

Not always. If a foreign freelancer does not have a permanent establishment or fixed place of business in the UAE, they are generally not subject to UAE corporate tax. However, each case depends on facts like physical presence, residency status, and business setup.

You must keep invoices, receipts, contracts, bank statements, expense records, and any agreements related to your work. From 2026 onward, records must be maintained for at least 7 years. Failure to provide them during an audit can result in penalties.

All business income is combined. Consulting, sponsored content, affiliate sales, digital products, or online courses — it all counts toward your total turnover and taxable profit. It is not calculated separately per platform.

No. They are separate systems.

VAT registration is required if taxable supplies exceed AED 375,000.

Corporate tax registration is required if business turnover exceeds AED 1 Million.

You may need to comply with both.

Yes, if the expenses are genuinely related to your business. A reasonable portion of rent, utilities, internet, and phone bills may be deductible. Personal expenses are not allowed. Always keep clear documentation.

Not every freelancer will be audited. However, you must maintain proper accounting records for at least 7 years. Under the 2026 documentation focus, the FTA may request records during surprise audits. Missing documents can trigger fines between AED 10,000 and AED 20,000.

Yes. If you are operating as a UAE-based freelancer, income earned from platforms like Upwork, Fiverr, Amazon, or other global marketplaces counts toward your gross turnover threshold.

It is based on gross turnover, not profit. That means total business revenue before deducting expenses. Even if your profit is low, registration is required once turnover crosses AED 1 Million.

Once registered, you must continue filing returns unless you qualify for deregistration and apply through the FTA. Simply earning less in a later year does not automatically cancel your registration.

No. Personal bank interest, savings returns, employment salary, and personal investments are excluded from business turnover calculations. Only income from your business activity is counted.

As of now, corporate tax law does not mandate specific e-invoicing software for freelancers. However, proper digital record keeping is strongly expected, and future digital compliance measures may increase. Staying organized electronically is highly recommended.

The fine will appear in your FTA account once imposed. Payment must be made through the FTA’s EmaraTax portal. In certain cases, you may submit a reconsideration request, but approval is not guaranteed.

Failure to update your registered details with the FTA may result in administrative penalties. Keeping your contact information updated is part of compliance obligations.

There is currently no standard “tax clearance certificate” required for all freelancers. However, you must deregister for corporate tax within 3 months of license cancellation. Failing to formally deregister can result in additional fines, even if you have stopped working.

References

- Federal Tax Authority. “Corporate Tax.” Government of the United Arab Emirates.

https://tax.gov.ae/en/corporate.tax.aspx - Ministry of Finance UAE. “Corporate Tax in the UAE.” https://mof.gov.ae/corporate-tax/

- Federal Tax Authority. “Corporate Tax Guide for Natural Persons.”

https://tax.gov.ae/data/Corporate-Tax-Guide-Natural-Persons.pdf - Federal Tax Authority. “Small Business Relief.” https://tax.gov.ae/en/small.business.relief.aspx

- PwC Middle East. “UAE Corporate Tax Overview.”

https://www.pwc.com/m1/en/services/tax/corporate-income-tax.html - KPMG UAE. “UAE Corporate Tax Regime: Key Considerations.”

https://home.kpmg/ae/en/home/insights/2022/01/uae-corporate-tax-regime.html - Deloitte Middle East. “UAE Corporate Tax: Frequently Asked Questions.”

https://www2.deloitte.com/xe/en/pages/tax/articles/uae-corporate-tax-faqs.html - EY UAE. “UAE Introduces Federal Corporate Tax.” https://www.ey.com/en_ae/services/tax

- Federal Tax Authority. “EmaraTax Portal.” https://eservices.tax.gov.ae/

- UAE Government Portal. “Corporate Tax Registration and Filing.”

https://u.ae/en/information-and-services/finance-and-investment/taxation/corporate-tax