Complete Guide to JAFZA Transfer Pricing & Corporate Tax in 2026

Zero tax doesn’t mean zero rules.

That’s the reality for businesses in JAFZA in 2026.

JAFZA remains one of the world’s most strategic trade zones — well-positioned, business-friendly, and still offering 0% corporate tax for qualifying companies. But that doesn’t mean it’s hands-off anymore.

The UAE has officially moved from a transitional education phase to an active, data-driven enforcement phase. 2026 marks the year of substantive audits.

This isn’t just about rates. It’s about how your group transactions are priced, documented, and disclosed — even if you’re not paying any tax.

Still wondering:

“If I owe 0%, why should transfer pricing matter?”

Here’s the reality: You’re not exempt.

Even at 0%, the Federal Tax Authority (FTA) expects clear records, arm’s length pricing, and clean disclosures.

The rules apply. The audits are real. The risk is high if you’re not ready.

If you’re running a JAFZA business, understanding how this works is no longer optional. It’s essential.

So what exactly are your obligations? And how do JAFZA companies navigate this without tripping over new UAE transfer pricing regulations?

This Jebel Ali Free Zone tax guide sets out how JAFZA corporate tax 2026, JAFZA transfer pricing rules, and the wider UAE free zone corporate tax regime now work together in practice.

Let’s break it down.

2026 Quick Fact:

0% corporate tax status is now strictly conditional on maintaining audited financial statements — regardless of revenue size.

Legal Framework for JAFZA Entities

If your company is based in JAFZA, you are automatically within the scope of the UAE Corporate Tax Law and the broader UAE free zone corporate tax framework, even if you’re currently paying 0% tax. This is a common point of confusion, so let’s break it down step by step.

The Law That Started It All

The UAE Corporate Tax Law, officially known as Federal Decree-Law No. 47 of 2022, applies to all businesses in the UAE, including free zone companies.

However, the law allows certain free zone businesses to pay 0% tax, but only if they meet specific conditions. These businesses are called “Qualifying Free Zone Persons” (QFZPs).

So, you’re not automatically exempt. You must qualify for the 0% rate.

What Does It Take to Be a Qualifying Free Zone Person (QFZP)?

According to Ministerial Decision No. 229 of 2025 (The Third Generation Free Zone Regulations), a JAFZA company can be treated as a QFZP if it meets all of the following:

- It earns “Qualifying Income”

- Income from doing business with companies outside the UAE, or

- Income from transactions with other free zone businesses (in specific circumstances), or

- Certain regulated activities (like warehousing, fund management, or logistics)

- It has enough substance in the UAE

- This means your business must have real operations

- You need employees, office space, and actual activity in the free zone.

- It prepares and keeps audited financial statements

- It does not conduct too much “non-qualifying” activity, such as selling directly to UAE mainland customers (unless done through a mainland branch, which is taxed at 9%).

If any one of these conditions is not met, your business loses QFZP status and becomes subject to the regular 9% corporate tax on all taxable income.

Where Do These Rules Come From?

Let’s connect the dots to the actual documents:

| Law / Decision | What it Covers |

| Federal Decree-Law No. 47 of 2022 | The main corporate tax law covers who pays tax, how much, and when |

| Ministerial Decision No. 229 of 2025 | Defines “Qualifying Income” for free zone companies under the updated 2026 free zone framework |

| Ministerial Decision No. 97 of 2023 | Explains what income is exempt from tax (e.g., dividends, capital gains) |

| Cabinet Decision No. 55 of 2023 | Lays out recordkeeping rules, accounting methods, and financial thresholds |

| Federal Decree-Law No. 17 of 2025 | Amends the Tax Procedures Law and introduces a hard 5-year expiry period for tax refunds and credits |

Together, these documents form the legal backbone for how corporate tax and exemptions apply to JAFZA companies.

The 5-Year Statute of Limitations

Under Federal Decree-Law No. 17 of 2025, tax refunds and credits are now subject to a hard 5-year expiry rule. If a credit is not claimed within five years from the end of the relevant tax period, it can permanently lapse.

This means businesses carrying forward adjustments, overpayments, or potential credits must review their positions before the end of 2026 to avoid losing entitlement.

Transfer Pricing Rules Also Apply — Even at 0%

Here’s where many JAFZA companies are getting caught off guard.

Even if your income is 100% qualifying and you pay 0% corporate tax, the JAFZA Transfer Pricing (TP) rules under Article 34 of the Tax Law still apply to you.

This means:

- If your company does business with related parties (like a parent company abroad, or other group entities),

- You must price those transactions fairly, as if they happened between unrelated parties,

- And you must keep proper documentation to prove that.

Why? Because the tax authorities want to make sure companies aren’t shifting profits or undercharging/overcharging group companies to avoid tax.

So yes, JAFZA transfer pricing compliance is mandatory, even if you’re at 0%.

Understanding Qualifying Free Zone Person (QFZP) Status

If your company is in JAFZA, you may be able to pay 0% corporate tax. But only if you qualify.

That’s where Qualifying Free Zone Person (QFZP) status comes in.

This status is not automatic. It comes with conditions. And if you don’t meet them, even once, you lose the 0% rate and get taxed at 9% like everyone else.

Let’s break down what QFZP means, how to get it, and how to keep it.

What Is a QFZP?

A QFZP is a company registered in a UAE free zone, like JAFZA, that qualifies for special tax treatment. The UAE Corporate Tax Law says that a QFZP pays:

- 0% tax on “qualifying income”

- 9% tax on “non-qualifying income”

The key point is that you must meet certain legal and operational conditions to be treated as a QFZP. If you don’t, your full income may be taxed at 9%.

What Counts as “Qualifying Income”?

The law splits income into two types:

- Qualifying Income (taxed at 0%)

- Income from selling goods or services to customers outside the UAE

- Certain income from other free zone businesses

- Some regulated activities (like logistics, fund management, or holding companies)

- Income from selling goods or services to customers outside the UAE

- Non-Qualifying Income (taxed at 9%)

- Sales made directly to UAE mainland customers (unless through a mainland branch)

- Unapproved activities not on the list of “qualifying activities”

- Income where the other party is related and outside the rules

- Sales made directly to UAE mainland customers (unless through a mainland branch)

If you earn both types of income, you must keep them clearly separated in your accounting. If you don’t, the FTA may tax your entire income at 9%, even if most of it should be 0%.

The AED 375,000 Threshold

The first AED 375,000 of your total taxable income is not taxed; this applies to all UAE businesses.

But this threshold doesn’t protect you if you fail to qualify for 0%. If you’re not a QFZP, your profit above AED 375,000 is taxed at 9%, and you won’t get the 0% rate on anything.

What You Need to Qualify

To get and keep QFZP status, your company must:

- Earn qualifying income (as explained above)

- Have real business operations in the free zone — not just a license

- Have people, premises, and expenses that match what you do

- Prepare audited financial statements each year

- Prepare audited financial statements each year — Mandatory under Ministerial Decision No. 84 of 2025 for all tax periods starting on or after 1 June 2023

- Elect QFZP status in your tax return (this is a formal step)

- Keep separate records for different types of income

If you fail any one of these, the FTA can cancel your QFZP status for that year. Under the current rules, this can also trigger a four-year exclusion period from requalifying. And once it’s gone, you can’t get it back mid-year.

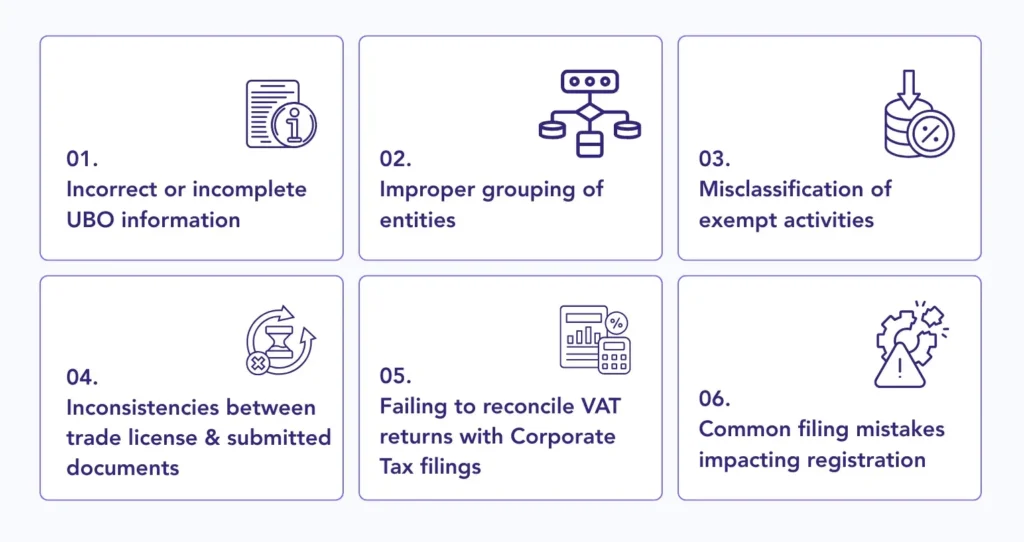

Common Mistakes That Cost You the 0%

Some businesses lose QFZP status without realizing it. These are the mistakes to avoid:

- Selling to UAE mainland customers directly from a free zone company, this is non-qualifying income.

- Not separating qualifying and non-qualifying income, the FTA might treat everything as taxable.

- Forgetting to check the QFZP box in the tax return, without it, you’re taxed at 9% by default.

- Skipping audited financials is a legal requirement. Under Ministerial Decision No. 84 of 2025, failure to maintain audited financial statements automatically jeopardizes QFZP eligibility.

- Having no real presence, the FTA checks if your company exists beyond paper.

The Penalty for Disqualification

If a JAFZA company fails to meet any QFZP condition in 2026, it is disqualified for that tax period and may be barred from requalifying for the next four tax periods.

This means the 0% benefit can effectively disappear for up to five years, and the company’s entire taxable income becomes subject to 9% corporate tax during that period.

Losing QFZP Status Has a Serious Impact

If you lose your QFZP status:

- Your entire income, not just the non-qualifying part, is taxed at 9%

- You can’t re-qualify until the next financial year — and under the four-year exclusion rule, re-entry may be blocked beyond just one year

- You could trigger group-level tax issues if your structure relies on that 0% rate

Transfer Pricing Applicability to JAFZA

Many JAFZA companies assume that if they qualify for 0% tax, UAE transfer pricing regulations don’t apply.

That’s incorrect.

The UAE transfer pricing regulations apply to all businesses, including free zone companies and those that pay no tax. This is confirmed by the Federal Tax Authority (FTA) in its Transfer Pricing Guide.

We are now firmly in the Audit Era — the focus has shifted from awareness to active review and risk-based selection through EmaraTax.

The law is not about how much tax you pay. It’s about how fairly you price your transactions with related parties.

When Does Transfer Pricing Apply?

If your company does business with related parties or connected persons, UAE transfer pricing regulations apply.

Related parties can include:

- A parent company or subsidiary

- Another company in the same group

- A company controlled by the same shareholders

- A director, shareholder, or close relative doing business with the company

These are called controlled transactions. The pricing for these deals must be set as if the parties were independent. This is called the arm’s length principle.

Key Thresholds You Should Know

JAFZA Transfer pricing rules apply to everyone, but some requirements depend on the size of your business and your transactions.

Here’s what you need to check:

- If your UAE group has an annual turnover above AED 200 million, or

- If your total related-party transactions exceed AED 40 million in aggregate in a tax year (as reflected in the 2026 CT-1 Return Disclosure thresholds)

In either case, you must prepare two documents:

- A Master File — covering the global group’s structure, functions, and pricing policies

- A Local File — covering your UAE entity’s related-party transactions

These are not optional once you cross the thresholds.

Disclosure Is Mandatory, even at 0%

Even if you don’t cross the thresholds, you still need to complete a Transfer Pricing Disclosure Form. This Disclosure Form is now fully integrated into the EmaraTax CT-1 Corporate Tax Return.

It asks for:

- A list of related parties

- The types and value of transactions

- Whether you prepared a Master File and a Local File

- The methods you used to price your transactions

This applies to all businesses that have related-party dealings, including Qualifying Free Zone Persons (QFZPs).

Connected Person Rules

There’s another threshold to keep in mind. If you pay a connected person (such as an owner, shareholder, or relative) more than AED 500,000 in aggregate during a tax year (as per the 2026 CT-1 schedule requirements), you must disclose it in a separate schedule.

This includes salaries, rent, consulting fees, and similar payments. These payments also need to be at market value.

Common Misconceptions

Here’s what many businesses get wrong:

- Thinking 0% tax means exemption from transfer pricing. It doesn’t. The law still applies.

- Believing small or informal group transactions won’t be noticed. In the Audit Era, automated risk filters review disclosure data against filed financials. They will, and must be reported.

- Assuming that UAE transfer pricing regulations are only for large multinational companies. It’s not. Many SMEs are caught by these rules.

Why It Matters

The FTA doesn’t just want to know your profits. It wants to know how you got there.

If your group deals aren’t priced properly, or if you don’t disclose them, you risk:

- Penalties for non-compliance

- Audits and investigations

- Losing QFZP status

- A 9% tax on your full income

Transfer pricing is now a permanent part of doing business in the UAE, including in free zones. The tax rate might be zero, but the rules are not.

Controlled Transactions Common in JAFZA

JAFZA Transfer pricing is not just a paperwork issue. It starts with the actual transactions your company does, especially with related companies inside or outside the UAE.

These are called controlled transactions. And in JAFZA, they’re common.

Many companies in this zone operate as part of larger regional or international groups. That means trade, logistics, shared costs, and intellectual property often flow across group lines.

Here’s a breakdown of the most frequent controlled transactions and how UAE transfer pricing regulations apply.

1. Import and Export with Foreign Affiliates

Many JAFZA companies import raw materials or finished goods from group companies abroad, then re-export them.

These are related-party transactions. You must ensure the pricing used for buying or selling is set at arm’s length, as if the parties were unrelated.

Why it matters: If prices are too low or too high, profits may shift unfairly between jurisdictions. That’s exactly what UAE transfer pricing regulations are designed to prevent.

2. Resale to UAE Mainland Customers

Some JAFZA companies buy goods from foreign affiliates and then resell them to mainland UAE customers.

If the supply chain includes related parties, all steps in the chain need to be priced properly.

Note: If you sell to the UAE mainland without using a branch, that income becomes non-qualifying and taxable at 9%. But the pricing of each step must still follow UAE transfer pricing regulations, especially if your supplier is a related party.

3. Shared Services: HR, IT, Finance

It’s common for group companies to centralize admin functions. For example:

- One company handles payroll and hiring for the group

- A regional head office provides IT infrastructure

- Finance teams are shared between subsidiaries

If your JAFZA company receives these services or provides them, you must charge or pay a fair, arm’s length fee. That usually means applying a cost-plus method, with markup based on what third parties would charge.

This must also be disclosed in your Transfer Pricing Disclosure Form.

4. Warehousing and Logistics Services

JAFZA businesses often operate group-level warehousing or supply chain hubs.

If one company uses another’s warehouse, picks and packs goods, or arranges transport, that’s a service. And that service needs a charge.

The fee must reflect market rates. Free or underpriced warehousing between group companies raises red flags under UAE transfer pricing regulations.

Under Ministerial Decision No. 229 of 2025, activities such as prepayment arrangements, factoring, and warehouse receipt financing are now expressly treated as qualifying activities within structured supply chain and financing models.

If your JAFZA entity operates as a distribution or logistics hub and more than 51% of its total revenue is derived from distribution activities, the qualifying income treatment and pricing expectations may shift, especially for commodity-linked flows.

5. Structured Commodity Financing

JAFZA entities involved in commodity trading often structure transactions using advance payments, back-to-back contracts, factoring arrangements, or warehouse receipt financing.

These arrangements are now specifically scrutinized under Ministerial Decision No. 229 of 2025, which recognises prepayment, factoring, and warehouse receipt financing within qualifying frameworks — but only if pricing remains arm’s length and commercially justifiable.

If financing margins, discount rates, or embedded service fees are not benchmarked properly, the FTA may recharacterise part of the income.

6. Use of Intellectual Property and Royalties

Some JAFZA entities hold trademarks or license rights from a group parent.

If you use a group of Intellectual Property — a brand name, software license, or product design, you must pay a royalty or license fee. And that rate needs to be justified.

Royalties are high-risk from a transfer pricing perspective. The FTA may request transfer pricing benchmark studies or documentation to prove the rate is reasonable.

Trading of Qualifying Commodities & Quoted Prices

For entities trading qualifying commodities, quoted market prices (such as exchange-referenced prices) may be used as a benchmark — but adjustments for transport, insurance, quality, and timing must still be documented.

If a JAFZA distribution hub exceeds the 51% revenue test for distribution activities, the analysis must clearly distinguish between pure trading margins and embedded service or financing elements.

Failure to segment these components can lead to adjustments under UAE transfer pricing regulations.

Why This Matters

The FTA is not just looking at your tax rate; it’s looking at how your group operates. If money or services flow between group companies, you must show:

- What was received and by whom

- Who paid what and to whom

- How was the price set

- Why was the pricing fair

Even if you’re a QFZP at 0%, these rules still apply.

Applying Transfer Pricing Methods to JAFZA Entities

Knowing the rules is one thing. Applying them correctly is another.

In JAFZA, where many businesses operate within multinational groups, the choice of Transfer Pricing (TP) method matters. The method you pick must reflect your actual function and risk. It also needs to be defendable.

The UAE Transfer Pricing Guide lists five accepted methods. But not all are equal in practice. Some are used more frequently than others, especially in free zone setups like JAFZA.

Let’s break it down.

Common TP Methods for JAFZA Companies

Here are the three most relevant methods for businesses operating in JAFZA:

1. Transactional Net Margin Method (TNMM)

Best for: Trading entities and distributors

TNMM is the most commonly used method for JAFZA companies that buy and sell goods, especially when pricing can’t be compared directly. It looks at your net profit margin against similar companies performing similar functions.

Example:

A JAFZA-based company imports electronics from its parent in Europe and resells them regionally. There’s no exact market price to compare the imports to. TNMM works well here by comparing the distributor’s margin against independent benchmarks.

2. Cost-Plus Method

Best for: Logistics providers, warehousing, and shared services

This method adds a standard markup to costs. It’s ideal when one entity provides routine services or support to others in the group.

Example:

A JAFZA company runs a warehouse used by other affiliates. It charges each one based on actual storage costs, plus a markup of, say, 5%–10%, depending on the service.

This method works best when the provider takes low risk and performs limited functions.

3. Comparable Uncontrolled Price (CUP) Method

Best for: Royalty payments, licensing, or straightforward goods trading

CUP compares the price charged between related parties to the price charged between unrelated ones. It’s simple, but only works if you have solid comparable data.

Example:

If your JAFZA entity licenses a trademark from a parent company, and the same trademark is licensed to third parties, CUP can be used to test if the internal rate is fair.

For commodity trading transactions, the CUP analysis now requires the use of a “Quoted Price” from a Recognized Price Reporting Agency, as mandated under Ministerial Decision No. 230 of 2025.

Recognized agencies include sources such as S&P Global Platts and Argus, and the quoted market price must be adjusted only for commercially justifiable differences such as transport, quality, and timing.

But usable third-party data is often hard to find, so while CUP is ideal in theory, it’s not always practical.

Choosing the Right Method

There’s no one-size-fits-all. Your choice depends on:

- The functions your JAFZA company performs

- The risks it takes on

- Whether there are comparable transactions or market data

- The type of relationship with the related party

2026 Benchmarking Case Study: JAFZA Resale to a Public Benefit Entity

Let’s say your JAFZA company resells industrial equipment sourced from a group company, and in 2026, it supplies part of that equipment to a Public Benefit Entity (as now recognized under Ministerial Decision No. 229 of 2025).

You choose TNMM to test whether your net margin is in line with the market. Here’s a simple benchmark analysis:

Your JAFZA entity’s margin: 4.3%

| Company | Function | Net Margin (%) |

| Company A | Independent trader | 3.6% |

| Company B | Regional distributor | 4.5% |

| Company C | Equipment reseller | 4.0% |

Since your margin is within the range of the comparables (3.5%–4.2%), the pricing is considered to be at arm’s length.

That’s how transfer pricing benchmarks support your Transfer Pricing method.

Why This Matters

Transfer Pricing documentation isn’t just about compliance. It’s your defense.

The FTA expects you to:

- Select the method that best fits your facts

- Apply it consistently

- Support it with transfer pricing benchmarks or internal data

Using the wrong method or applying the right one incorrectly can lead to adjustments, penalties, and disputes.

Therefore, for accurate benchmarking and method selection, many businesses rely on professional transfer pricing services to ensure compliance and reduce audit risk in JAFZA.

Documentation Requirements & Filing Timeline

Transfer pricing compliance doesn’t stop at picking the right method. You also need to document everything and file it on time through the EmaraTax portal.

Even if your company is based in JAFZA and qualifies for 0% corporate tax, transfer pricing documentation and disclosure are still required.

Let’s break it down.

The Three Key Documentation Requirements

Here are the main documents the UAE Transfer Pricing regime requires:

- Transfer Pricing Disclosure Form

- Must be filed with the Corporate Tax Return

- Mandatory for any business that has related-party or connected person transactions, regardless of size

- Lists all related parties, transaction values, and methods used

- Must be filed with the Corporate Tax Return

- Local File

- Contains a detailed analysis of your UAE entity’s transactions

- Includes functional analysis, contracts, benchmarking, and method application

- Required if:

- Your UAE consolidated group revenue exceeds AED 3.15 billion, and

- Your total related-party transactions exceeded AED 50 million during the tax year

- Your UAE consolidated group revenue exceeds AED 3.15 billion, and

- Contains a detailed analysis of your UAE entity’s transactions

- Master File

- Provides an overview of the entire multinational group

- Includes group structure, global pricing policies, IP ownership, and financing

- Required under the same thresholds as the Local File

- Provides an overview of the entire multinational group

Note: The Local File and Master File must now be maintained in an Audit-Ready state and must be provided within 30 days of an FTA request.

Filing Timeline

Your company’s Corporate Tax Return and Transfer Pricing Disclosure Form must be filed within 9 months after the end of your financial year.

If your financial year ends on 31 December 2025:

- Corporate Tax Return + TP Disclosure Form → Due by 30 September 2026

- Local and Master Files → Must be ready by the same date and maintained in Audit-Ready format

These timelines are strict. Late filing can trigger penalties.

EmaraTax Portal: What You Need to Know

The FTA’s EmaraTax platform is the central system for filing both your Corporate Tax Return and the Transfer Pricing Disclosure.

Key features to be aware of:

- Auto-populated fields based on previous submissions and license data

- Drop-downs for selecting related parties and transaction types

- Mandatory fields for method selection and arm’s length confirmation

- Elections must be made during return filing (e.g., choosing QFZP status)

- Transaction value schedules must match what’s in your financials

This system leaves little room for error. Everything you submit is cross-checked by logic rules.

E-Invoicing Readiness for July 2026

The UAE Electronic Invoicing System (EIS) pilot is scheduled to launch in July 2026, introducing structured digital reporting between taxpayers and the FTA.

Businesses with annual revenue exceeding AED 50 million are expected to onboard through an Accredited Service Provider (ASP) to transmit invoice data in real time or near real time.

This means transfer pricing transaction values, especially related-party supplies, must reconcile with e-invoicing data once the system becomes operational.

Common Mistakes to Avoid

Many companies make the same filing errors. Here are the ones that can cost you:

- Failing to check the QFZP election box — this defaults you to full 9% tax

- Mismatched transaction values — if your TP form doesn’t align with your return or financials, it raises a red flag

- Leaving out connected persons — even if payments are small, some still require disclosure

- Missing the deadline — 9 months might seem long, but benchmarking and file prep takes time

- Assuming 0% tax means no documentation — even QFZPs must disclose transactions and justify pricing

Why This Matters

The FTA is building a data-driven audit system. If your filings don’t match, or if documentation is missing, your company could be selected for review.

And if you can’t produce your Master File or Local File when requested?

That’s a compliance failure, and it comes with consequences.

Common Risks & Penalties

JAFZA Transfer pricing compliance isn’t just about checking boxes. If it’s done wrong — or not done at all — the consequences are real.

The Federal Tax Authority (FTA) has made it clear: 2026 marks the shift into an enforcement-driven environment under Cabinet Decision No. 129 of 2025.

Let’s go over the key risks, audit triggers, and 2026 penalties that JAFZA companies need to avoid.

Risk 1: Improper Benchmarking

Benchmarking is not optional — it’s what backs up your pricing.

The most common mistake? Using weak or irrelevant comparables. That includes:

- Comparing against unrelated industries

- Ignoring regional market differences

- Using outdated or unaudited financial data

FTA expects clean, consistent, and localised benchmarks. Anything less, and they may disregard your method entirely — which can now trigger interest exposure under the 14% Annual Interest Rule.

Risk 2: Misclassifying Related Parties

Another frequent error: failing to declare or correctly label related parties and connected persons.

Examples:

- Omitting sister companies or entities under common ownership

- Failing to disclose transactions with shareholders or board members

- Treating connected-person salaries or perks as routine expenses

FTA guidance — and audit experience — shows that misclassification is one of the top red flags. If misclassification results in underpayment of tax, interest accrues from the original due date.

Risk 3: Disclosure Form Errors

The Transfer Pricing Disclosure Form is a key document. Mistakes here are costly.

FTA is flagging forms that:

- Omit required transactions

- Don’t match the financial statements

- Fail to declare elections (like QFZP status)

- Leave out payment details to connected persons

Errors, inconsistencies, or vague answers can lead to audits and any resulting tax shortfall is subject to 14% annual interest calculated monthly.

Risk 4: Excessive Service Charges

Service transactions within groups are a major audit focus.

FTA is reviewing:

- Shared service fees with no clear cost basis

- Management fees that seem inflated

- Group support services with no supporting documentation

If you’re charging or paying for services, you need proof of benefit, cost breakdowns, and markup rationale. If it’s not real, or not priced fairly, the FTA can adjust or disallow it, and unpaid differences accrue monthly interest.

Risk 5: Below-Market Margins

If your JAFZA company is earning margins that fall below the arm’s length range — especially if you’re a distributor or service provider — expect scrutiny.

FTA may argue:

- You’re shifting profits out of the UAE

- You’ve underreported taxable income

- You’ve incorrectly applied the TP method

And they can re-calculate your taxable profit accordingly — with interest running at 14% per annum, applied monthly, from the original filing deadline.

The 14% Annual Interest Rule (Effective 14 April 2026)

Under Cabinet Decision No. 129 of 2025, unpaid Corporate Tax is now subject to 14% annual interest, calculated monthly, from the original due date until settlement.

Late Voluntary Disclosures are subject to an additional 1% monthly penalty on the unpaid tax difference.

The previous 300% penalty cap for late payments has been removed under the interest-based framework, meaning exposure can continue to grow over time.

What Are the Penalties?

Here’s what’s on the line:

- Failure to submit the TP Disclosure Form: AED 10,000

- Failure to provide TP documentation on request: AED 20,000–30,000

- Inaccurate returns or misleading information: Higher penalties or audits

- Transfer pricing adjustments by FTA: Additional 9% tax + interest + penalties

- Loss of QFZP status: Full-year corporate tax at 9%

FTA is building a data-driven compliance system. Once you’re flagged, it’s hard to undo.

2025 vs. 2026 Penalty Framework

| Aspect | 2025 Framework | 2026 Framework (Effective 14 April 2026) |

| Late Payment Structure | Fixed administrative fines | 14% p.a. interest calculated monthly |

| Voluntary Disclosure | Percentage-based penalties | 1% monthly on unpaid tax difference |

| Penalty Cap | 300% cap applied | No traditional 300% cap — interest continues until payment |

| Audit Adjustment Impact | Additional tax + fines | Additional tax + ongoing interest accumulation |

JAFZA Holding Companies and TP Exposure

JAFZA holding companies are often used to centralise ownership, IP, financing, or management functions across group entities. But that setup brings higher transfer pricing (TP) exposure, and, increasingly, Global Minimum Tax and Domestic Minimum Top-Up Tax (DMTT) scrutiny.

As the UAE aligns with OECD Pillar Two and global minimum tax standards, JAFZA holding structures face new compliance risks. From 2025/2026, large multinational groups are subject to a 15% minimum tax in the UAE under the Domestic Minimum Top-Up Tax (DMTT) regime. If your group crosses key thresholds, transfer pricing is no longer just a local issue; it becomes a global one.

Why JAFZA Holding Companies Attract TP Scrutiny

Holding companies in JAFZA are often used for:

- Owning intellectual property (IP) and licensing it to operating entities

- Providing intercompany financing (loans, guarantees, cash pooling)

- Charging group-wide management or admin fees

- Consolidating treasury, legal, HR, or strategic functions

All these involve controlled transactions, and all are under FTA OECD watch, and Pillar Two / DMTT watch.

The key question: Are these activities real and active, or just paper functions?

If the FTA sees a holding company with no substance, yet collecting large fees or royalties, it can challenge the entire arrangement — and under DMTT rules, low-tax income may be topped up to 15% in the UAE itself.

Master File, CbCR & Group Reporting Thresholds

If your UAE consolidated revenue exceeds AED 3.15 billion, your group may be subject to:

- Master File: Describes the global business, IP, financing, and tax policies

- Country-by-Country Reporting (CbCR): Discloses where profits, tax, and employees are located

- Local File: Discloses transaction-level TP details for UAE entities

Holding companies must be ready to justify their functions, assets, and risk, not just their revenue streams. Otherwise, intercompany income (like interest or royalties) may be recharacterized, and any shortfall below 15% effective tax rate may trigger DMTT top-up tax locally.

DMTT: The End of 0% for Global Giants

For multinational groups with consolidated revenue exceeding EUR 750 million, the UAE’s Domestic Minimum Top-Up Tax (DMTT) ensures a 15% minimum effective tax rate starting in 2025/2026.

This means that even if a JAFZA holding company qualifies for 0% under the Corporate Tax Law as a QFZP, large groups will not remain at 0% once DMTT applies.

The tax is calculated using Pillar Two (GloBE) methodology, based on financial accounting income with specific adjustments.

The 0% regime continues to apply legally, but any gap between the effective tax rate and 15% will be topped up under DMTT.

Pillar Two and the Global Minimum Tax

The UAE is preparing to implement Pillar Two under the OECD’s GloBE (Global Anti-Base Erosion) framework. That means:

- Multinational groups with revenue over EUR 750 million may be subject to a 15% minimum effective tax

- Low-tax income (including 0% income in free zones) could trigger top-up taxes — but now through the UAE’s Domestic Minimum Top-Up Tax instead of foreign jurisdictions.

- In early 2026, the Side-by-Side (SbS) Safe Harbor framework was introduced, allowing qualifying groups to rely on simplified calculations if they meet specific effective tax rate and reporting conditions.

- The SbS Safe Harbor is not automatic. Groups must assess eligibility annually and maintain consistent data alignment between Corporate Tax, CbCR, and GloBE reporting.

- JAFZA holding companies — especially IP owners and finance hubs — are now in scope

Even if you qualify as a QFZP in the UAE, your group’s parent or intermediate entities may owe tax in other jurisdictions due to GloBE rules.

GloBE Readiness: What JAFZA Holding Entities Need to Do

- Identify high-risk income streams

- IP licensing, group loans, management fees, and any 0% income with minimal substance

- IP licensing, group loans, management fees, and any 0% income with minimal substance

- Assess substance vs. form

- Do you have local employees, decision-makers, and real economic activity?

- Do you have local employees, decision-makers, and real economic activity?

- Align documentation with Pillar Two expectations

- Update Master Files and Local Files to reflect actual functions and risk

- Make sure intercompany payments are benchmarked and defendable

- Update Master Files and Local Files to reflect actual functions and risk

- Prepare for IPE (International Permanent Establishment) elections

- Some holding companies may need to elect for certain reporting or tax treatments under GloBE

- Some holding companies may need to elect for certain reporting or tax treatments under GloBE

- Coordinate with the group’s global tax team

- TP decisions made in JAFZA can impact group-level top-up tax exposure

JAFZA Holding Companies and TP Exposure

JAFZA holding companies play a central role in many UAE-based group structures. They often control IP, issue intercompany loans, or manage regional operations from a low-tax platform.

That structure makes sense commercially. But it also triggers higher transfer pricing (TP) and global tax risk.

Common Holding Company Activities Under Scrutiny

The following activities, when done between group entities, fall directly under TP rules:

- IP licensing: Charging royalties to operating companies

- Intercompany financing: Lending, guarantees, and treasury support

- Centralised services: Group-level HR, finance, legal, IT or leadership functions

These aren’t passive activities. They require substance and fair pricing.

If your JAFZA entity receives large income from these functions but shows limited operations or people on the ground, the Federal Tax Authority (FTA) will ask questions. Under a DMTT environment, those questions don’t just impact 0% status — they influence whether a 15% minimum effective tax applies to that income.

TP Documentation Risk: Local File, Master File, and CbCR

If your UAE group’s consolidated revenue exceeds AED 3.15 billion, you face full-scale documentation rules:

- Local File: Detailed analysis of transactions involving UAE entities

- Master File: Global overview of your group’s business, functions, and transfer pricing

- Country-by-Country Report (CbCR): Tax, profit, and headcount by jurisdiction

For holding companies, these reports must justify the allocation of profits. If the UAE entity receives high income but performs few functions, the group could face reallocation or tax adjustments in other countries and potential DMTT top-up tax in the UAE if the effective tax rate falls below 15%.

Global Minimum Tax: Enter Pillar Two

The 0% tax advantage for holding companies won’t last forever.

The OECD’s Pillar Two rules, now being adopted by the UAE, will introduce a 15% global minimum tax for groups with annual revenue over EUR 750 million.

From 2025/2026, these groups are expected to face a 15% minimum effective tax in the UAE through the Domestic Minimum Top-Up Tax (DMTT), calculated under GloBE-style rules.

This changes the game for JAFZA structures.

Even if your holding company is a Qualifying Free Zone Person (QFZP) with 0% tax in the UAE, top-up tax could be charged elsewhere if:

- The entity earns passive income (like IP or interest)

- It lacks local substance

- The group’s Effective Tax Rate (ETR) in the UAE falls below 15% under GloBE rules

With DMTT, that top-up tax may now be collected in the UAE itself rather than in a foreign jurisdiction, aligning domestic rules with the Global Minimum Tax framework.

And this tax won’t hit just the holding company, it may hit the ultimate parent, intermediate parent, or a designated local entity.

The group must therefore monitor both GloBE and DMTT outcomes side by side, including whether it can rely on any emerging Side-by-Side (SbS) Safe Harbor simplifications announced in early 2026.

Preparing for GloBE and IPE Exposure

Multinational groups need to be ready.

Here’s what JAFZA holding entities should do now:

- Map out all controlled transactions: Royalty flows, loans, service fees, cost-sharing

- Review legal and operational substance: How many people are on payroll? Who makes decisions? Where is IP developed and managed?

- Ensure documentation aligns: Master File and Local File must reflect actual roles, not just tax positioning

- Benchmark everything: IP income, interest rates, service markups, all must be tested and defensible

- Coordinate with group tax teams: GloBE rules require global coordination. TP missteps in JAFZA can cause exposure at the parent level and now directly influence DMTT top-up tax computations in the UAE for groups above the EUR 750 million threshold.

ESR vs TP in JAFZA – What’s the Difference?

Many JAFZA companies think that if they comply with Economic Substance Regulations (ESR), they’ve also ticked the Transfer Pricing (TP) box.

That’s a mistake.

The two regimes are separate, apply in different situations, and require different actions.

In 2026, however, enforcement has moved into a phase of “Data Convergence,” where the FTA digitally cross-references ESR and Transfer Pricing filings.

When ESR Applies

ESR applies to specific business activities carried out in the UAE. These include:

- Holding company activities

- Headquarters or management services

- IP ownership and licensing

- Distribution and service centre operations

- Financing and leasing

- Shipping and fund management

If your company earns income from one of these Relevant Activities, you must:

- File an ESR Notification

- Submit an ESR Report

- Demonstrate adequate economic substance in the UAE — meaning staff, premises, and core decision-making

The focus of ESR is: Do you actually do business in the UAE, or are you just booking profits here?

In the current audit environment, the FTA automatically reviews ESR Core Income Generating Activities (CIGAs) alongside the functions disclosed in the Transfer Pricing Local File.

When Transfer Pricing Applies

TP rules apply to any transaction with related parties or connected persons, regardless of your industry or activity type.

It doesn’t matter if you’re a service company, a warehouse, or a holding entity — if you’re transacting with related entities, TP applies.

You must:

- Disclose the transactions

- Choose and apply an arm’s length pricing method

- Benchmark your pricing

- Prepare and maintain a Local File and Master File (if thresholds are met)

The focus of TP is: Is your pricing fair, as if the parties were unrelated?

In 2026, TP disclosures are increasingly reviewed in conjunction with ESR filings to detect inconsistencies in substance and profitability.

Key Differences

| Point | ESR | Transfer Pricing (TP) |

| What it covers | Specific income-generating business activities | Any transaction with related/connected parties |

| Who does it apply to | Companies engaged in “Relevant Activities” | All companies with controlled transactions |

| Test applied | Substance — people, premises, decision-making | Pricing — arm’s length, comparability |

| Main submission | ESR Report + Notification | TP Disclosure Form + Files |

| Thresholds | Based on activity and income | Based on group revenue & transaction size |

One Doesn’t Cover the Other

Just because your company meets ESR requirements, that does not mean your TP is compliant.

ESR only proves you have substance. It doesn’t prove your pricing is fair.

FTA and the Ministry of Finance treat both regimes separately. And both have their penalties. But under the current data-driven framework, they are reviewed together.

The “Consistency Gap” Audit Trigger

A major 2026 audit trigger is the “Consistency Gap.” This occurs when a company reports high profitability in its Transfer Pricing Local File but shows minimal or zero employees in its ESR report.

For example, if a JAFZA entity reports significant royalty or financing income in its TP file but declares limited CIGAs or personnel under ESR, the FTA may initiate an immediate desk audit.

High profits + low substance = automatic scrutiny.

Coordination Matters

That said, your ESR and TP disclosures must tell a consistent story.

For example:

- If you claim in ESR that your JAFZA entity manages IP, your TP file should show royalty income and explain how it’s priced.

- If your ESR says you employ finance staff, but your TP file shows zero service charges to affiliates, that’s a red flag.

Mismatch equals audit risk.

And in a data-converged environment, mismatches are detected automatically.

So your ESR team and TP team need to talk — especially when preparing disclosures and documentation.

Transfer Pricing Compliance Checklist for JAFZA Businesses

Transfer pricing is no longer a back-office task. For JAFZA entities, it’s now a core compliance requirement, with real tax and legal consequences if ignored.

Here’s a straightforward checklist to help your business stay fully compliant in 2026:

1. Corporate Tax Registration

- Ensure your JAFZA entity complies with the mandatory corporate tax registration in the UAE by completing the process through the EmaraTax portal.

- Even if your income is at 0%, registration is mandatory.

2. Confirm QFZP Eligibility and Monitor Income

- Check that your business qualifies as a Qualifying Free Zone Person (QFZP).

- Track your revenue streams closely — especially mainland transactions, passive income, or non-qualifying services.

- Make the QFZP election in your corporate tax return each year.

3. Identify Related and Connected Party Transactions

- Map out all controlled transactions — goods, services, IP, financing, management fees.

- Include payments to connected persons, such as owners, shareholders, and relatives.

- Keep this list updated and documented.

4. Conduct Benchmarking and Apply TP Methods

- Choose the most suitable TP method based on your function and risk.

- Run benchmarking studies annually, especially for key services, loans, and royalties.

- Document your logic — not just your numbers.

5. Prepare and File TP Documentation

- Submit the Transfer Pricing Disclosure Form along with your Corporate Tax Return.

- If your group revenue exceeds AED 3.15 billion, prepare a Local File and Master File.

- Make sure documentation is ready by the return deadline, even if not submitted.

6. Coordinate TP and ESR Submissions

- Ensure your ESR reports align with your TP disclosures.

- If ESR says you conduct HQ, IP, or finance activities, your TP file must reflect that — with pricing to match.

- Inconsistencies increase audit risk.

7. Use EmaraTax Correctly

- Ensure all elections, schedules, and declarations are accurate and complete.

- Avoid common mistakes:

- Leaving out related parties

- Failing to declare connected persons

- Mismatched transaction values

- Leaving out related parties

- Double-check every entry before submission.

8. Apply for an Advance Pricing Agreement (APA)

As of January 2026, the FTA accepts applications for both domestic and cross-border Advance Pricing Agreements (APAs) for controlled transactions exceeding AED 100 million.

The APA program carries an application fee of AED 30,000 and allows businesses to obtain upfront certainty on their transfer pricing methodology for covered transactions.

For large or high-risk intercompany arrangements, an APA can significantly reduce audit exposure and interest-based penalties.

9. Implement an Arabic Records Policy

Ensure key tax records, contracts, and documentation can be provided in Arabic if requested by the FTA.

Failure to maintain or provide required records in Arabic may result in administrative penalties of AED 5,000.

10. Build Internal Controls

- Assign ownership of TP compliance within your team.

- Create an internal calendar for key deadlines.

- Keep records, contracts, and calculations organised and accessible.

Note: Consider engaging expert transfer pricing services to handle documentation, EmaraTax filings, and method reviews, especially if your transactions are complex or cross-border.

FAQs:

Common red flags include vague service descriptions, missing benchmarking, mismatches between TP and ESR filings, and unexplained below-market margins—especially for large related-party payments. These are serious risk indicators under UAE transfer pricing regulations.

Yes. The 0% rate only applies to qualifying income. Transfer pricing still applies, and incorrect pricing, disclosures, or documentation, regardless of your corporate tax registration, can trigger penalties, audits, or even the loss of QFZP status.

Warehousing markups should be benchmarked using the cost-plus method, supported by regional comparables. Under UAE transfer pricing regulations, the FTA expects clear cost breakdowns, risk-adjusted margins, and documentation, often prepared with help from professional transfer pricing services.

Yes. Intercompany loans, guarantees, and treasury arrangements must reflect commercial terms and actual credit risk. Under UAE transfer pricing regulations, proper benchmarking and documentation are essential to avoid audit challenges.

Yes. EmaraTax includes automated validation. If connected parties, elections, or figures don’t align, the system may reject your return during corporate tax registration filing or flag issues for review.

Failing to submit the schedule can lead to penalties, increased audit scrutiny, and even loss of QFZP status. It signals weak compliance, even if other filings are correct, and may raise questions about transparency in related-party dealings.

Yes. If the group crosses the EUR 750M threshold, CbCR still applies, even for passive entities. Many firms rely on transfer pricing services to coordinate disclosures.

ESR focuses on real UAE presence, staff, governance, and decision-making. TP, on the other hand, tests whether intercompany pricing reflects market value. Both apply, but address different risks under UAE transfer pricing regulations.

If non-qualifying income goes over AED 375,000, the company loses its 0% tax benefit. The full income becomes taxable at a rate of 9%, making this threshold a crucial line that businesses must closely monitor to maintain QFZP status.

No. Free Zone Persons are not eligible for Small Business Relief. Transfer pricing in UAE applies even to low-revenue entities that conduct related-party transactions.

Yes, if the director is a connected person. Their compensation must be reasonable and in line with market standards. This is typically achieved through a thorough benchmarking analysis in transfer pricing, supported by clear documentation to prevent compliance issues.

Start with the CUP method if available. Otherwise, TNMM with value justification works. This area of transfer pricing in UAE often requires strong documentation and comparables.

FTA expects a clear analysis of functions, assets, and risks. If margins are low, your functional story must hold up. Many businesses engage transfer pricing services for this.

FTA may deny deductions or apply 9% tax if support is weak. Each recharge must be documented and benchmarked according to UAE transfer pricing regulations.

If income from mainland and Free Zone activities isn’t properly ringfenced, the entity risks losing its QFZP status. Accurate documentation and support from professional transfer pricing services are critical to meet compliance and avoid misclassification under UAE tax rules.

Yes. If group thresholds are met or related-party transactions exist, documentation is required, even if one entity is dormant. This is standard under transfer pricing in UAE.

Economic rationale ensures the transfer pricing method matches how the business truly works—what it does, what risks it takes, and what value it adds. Without that alignment, tax authorities may reject the method and question the reported profits.

EmaraTax automatically cross-checks your entries. If figures in the tax return don’t match those in the transfer pricing schedules, the system may flag the return, delay submission, or prompt a follow-up from the Federal Tax Authority.

Fees must be linked to actual services, with clear cost structures and markups. Unsubstantiated charges carry audit risk—transfer pricing services can help you benchmark and document these.

Outdated benchmarking weakens your position. The FTA expects current, relevant data that reflects today’s market. Using old or irrelevant comparables can lead to adjustments, penalties, and reduced credibility during audits or reviews of your transfer pricing documentation.

Yes — but only if you file your first Corporate Tax return within 7 months from the end of your tax period. Outside that window, a waiver is discretionary and not guaranteed by the FTA.

No. Under Cabinet Decision No. 129 of 2025 (effective 14 April 2026), unpaid Corporate Tax is subject to 14% annual interest calculated monthly, and it is not capped under the previous 300% administrative penalty framework.

Yes. Even if revenue is zero, audited financial statements are required to maintain QFZP 0% election eligibility. Without an audit, the 0% status may be denied.

The transitional window for claiming 2021 VAT credits closes on 31 December 2026. Claims submitted after this deadline may be rejected.

References

- Authority, Federal Tax. ‘Federal Tax Authority – United Arab Emirates’. Federal Tax Authority United Arab Emirates, https://tax.gov.ae//en/.

- Bot Verification. https://bcl.ae/corporate-tax-law-uae/#:~:text=CONNECTED%20PERSONS%20UNDER%20THE%20UAE%20TAX%20LAW%20INCLUDES&text=Kinship%20with%20Owner%2FDirector%2FOffice,marriage%2C%20adoption%2C%20or%20guardianship.

- Corporate Tax (CT). https://u.ae/en/information-and-services/finance-and-investment/taxation/corporate-tax.

- Determining Qualifying Income. https://tax.gov.ae/Datafolder/Files/Legislation/Cabinet%20Decision%20No.%20100%20of%202023%20on%20Determining%20Qualifying%20Income%20for%20the%20Qualifying%20Free%20Zone%20Person%20-%20for%20publishing.pdf.

- EmaraTax. https://u.ae/en/information-and-services/finance-and-investment/taxation/emaratax.

- Federal Decree-Law No. 47 of 2022.

https://mof.gov.ae/wp-content/uploads/2022/12/Federal-Decree-Law-No.-47-of-2022-EN.pdf. - Free Zone Persons. https://tax.gov.ae/Datafolder/Files/Guides/CT/Free%20Zone%20Persons%20-%2020%2005%202024%20final%20for%20GCD.pdf.

- Global Anti-Base Erosion Model Rules (Pillar Two). https://www.oecd.org/en/topics/sub-issues/global-minimum-tax/global-anti-base-erosion-model-rules-pillar-two.html.

- ‘Jebel Ali Free Zone’. Jebel Ali Free Zone (Jafza), https://www.jafza.ae/.

- Minimum Tax Implementation Handbook (Pillar Two). https://www.oecd.org/content/dam/oecd/en/topics/policy-sub-issues/global-minimum-tax/minimum-tax-implementation-handbook-pillar-two.pdf.

- Ministerial Decision No. 139 of 2023 R. https://mof.gov.ae/wp-content/uploads/2023/06/Ministerial-Decision-No.-139-of-2023-Regarding-Qualifying-Activities-and-Excluded-Activities.pdf.

- The Economic Substance Regulations. https://u.ae/en/information-and-services/finance-and-investment/taxation/the-economic-substance-regulations.

- TRANSFER PRICING APPLICATION OF THE ARM’S LENGTH PRINCIPLE . https://www.mira.gov.mv/Files/GetFile/ff5a98b8-d862-47c6-be59-3d19ed225e75.

- Abdou, Mahmoud. ‘Ministry of Finance to Implement Amendments to the Tax Procedures Law Starting Early 2026’. Ministry of Finance – United Arab Emirates, 29 Nov. 2025,

https://mof.gov.ae/en/news/ministry-of-finance-to-implement-amendments-to-the-tax-procedures-law-starting-early-2026/. - Advance Pricing Agreements. https://tax.gov.ae/Datafolder/Files/Guides/CT/APA-Guide-EN-30-12-2025.pdf.

- ‘eInvoicing’. Ministry of Finance – United Arab Emirates, https://mof.gov.ae/en/about-us/initiatives/einvoicing/.

- Ministerial Decision No. 84 of 2025 on Audited Financial Statements for the Purposes of Federal Decree-Law No. 47 of 2022 on the Taxation of Corporations and Businesses. https://mof.gov.ae/wp-content/uploads/2025/04/Ministerial-Decision-No.-84-of-2025-on-Audited-Financial-Statements.pdf.

- Ministerial Decision No. 229 of 2025 Regarding Qualifying Activities and Excluded Activities for the Purposes of Federal Decree-Law No. 47 of 2022 on the Taxation of Corporations and Businesses.

https://mof.gov.ae/wp-content/uploads/2025/09/EN-Ministerial-Decision-No.-229-of-2025-Regarding-Qualifying-Activities-and-Excluded-Activities.pdf. - Tax Challenges Arising from the Digitalisation of the Economy – Global Anti-Base Erosion Model Rules (Pillar Two), Side-by-Side Package.

https://www.oecd.org/content/dam/oecd/en/topics/policy-sub-issues/global-minimum-tax/side-by-side-package.pdf. - The UAE Economic Substance Regulations Guidance on Economic Substance Report.

https://mof.gov.ae/wp-content/uploads/2022/08/Guidance-on-Economic-Substance-Report-Guidance.pdf. - ‘Top-up Tax’. Ministry of Finance – United Arab Emirates,

https://mof.gov.ae/en/public-finance/tax/top-up-tax/.