Understanding ESP (ETIP): A Comprehensive Guide

Worried About High Electricity Bills in the UAE? Electricity bills in the UAE are no longer just a cost concern—they are now directly tied to mandatory environmental compliance and the May 30, 2026 deadline under UAE climate regulations. Electricity bills in the UAE are going up. Fast. At the same time, the country is enforcing its national mandates under Operation 300Bn and the Net Zero 2050 strategy, shifting from voluntary sustainability goals to legally binding requirements. Sounds great, right? But here’s the problem.

Power costs are rising so quickly, they can hurt your business before you even start. With the April 2026 fuel surcharge now averaging around 0.060/kWh across Dubai and similar rates applied by TAQA Distribution, energy costs are no longer predictable—they are regulated, monitored, and penalized if mismanaged. Green setups cost more in the beginning. Monthly bills are painfully high. Profit margins are crushed. That’s where the Energy Support Program (ESP), formerly known as ETIP, comes in.

ESP (ETIP) stands for Energy Support Program.

It’s designed to help businesses, especially in the industrial and manufacturing sectors—cut down electricity costs. Lower costs. Higher profits. Simple as that.

If you’re planning to launch a business in the UAE, this is something you can’t ignore.

Skip it now, and your power bills could eat into your profits later. So let’s make it easy.

As of 2026, energy efficiency is no longer a choice; it is a legal requirement for all UAE-based industrial sources. Non-compliance with Federal Decree-Law No. 11 of 2024 can result in penalties of up to AED 2,000,000 for failure to report emissions data and meet mandatory thresholds.

What is ESP formerly known as ETIP? How does it work? And why could it be the smartest move for your business? Let’s break it down.

The 2026 Compliance Pivot: Why Participation is Mandatory

The Energy Support Program is no longer just a cost-saving initiative. It is the operational backbone of the UAE’s Monitoring, Reporting, and Verification (MRV) system introduced in October 2025. Businesses are now required to maintain real-time, auditable energy data, not just annual utility bills.

Failure to align with ESP means more than losing tariff benefits. It exposes businesses to regulatory scrutiny, loss of tax incentives, and potential restrictions on industrial licensing—especially in high-demand zones prioritizing compliant entities.

What is ETIP?

The Energy Support Program (ESP), formerly known as ETIP, represents the UAE’s unified framework for industrial energy efficiency, tariff optimization, and regulatory compliance under its national decarbonization strategy. It helps energy-heavy businesses cut electricity costs. The UAE launched this program to make sure industries stay sustainable and cost-efficient. The goal? Use energy better while keeping the UAE a top choice for business.

Running a factory in the UAE isn’t cheap. Electricity bills can skyrocket. ESP offers lower electricity rates to eligible companies. But ESP isn’t just about saving money. It’s part of a bigger plan to make industries smarter and more efficient.

The Ministry of Industry and Advanced Technology (MoIAT) is enforcing the industrial decarbonization roadmap. They’re working with key partners like:

- Department of Energy (DoE) in each emirate

- TAQA Distribution (replacing ADDC/AADC under the unified 2025 restructuring)

- Local utility providers (e.g., ADDC, DEWA, SEWA)

- Ministry of Climate Change and Environment (MOCCAE) as a primary stakeholder in emissions evaluation and MRV integration

- Other local authorities responsible for approving and implementing the tariff reductions

For 2026 eligibility, companies are assessed based on connected load thresholds and operational maturity. “Existing companies” are those operational for more than 6 months, while “new companies” must demonstrate projected compliance under the same framework. Connected load scoring—particularly for facilities above 5MW—directly impacts tariff eligibility and compliance classification.

Why ESP Matters for UAE Businesses

Energy means a major business cost. And in the UAE, where power demand is high, smart energy decisions can make or break your bottom line. Here’s why ESP is a strategic advantage.

Lower Electricity Bills

This is the big one. ESP gives reduced electricity tariffs to qualifying businesses. That means lower operating costs and higher profit margins, especially for energy-hungry operations like factories or data centers.

Under the 2026 framework, tariff benefits are structured into performance-based categories:

| ESP Score Category | Score Range | 2026 Electricity (Fils/unit) | 2026 Gas (AED/MBTU) |

| Category A | ≥ 80% | 20 | 7.9 |

| Category B | 60% – 79% | 22 | 9.1 |

| Category C | 50% – 59% | 25 | 10.3 |

| Standard Tariff | < 50% | Variable (Market Rate) | Variable |

Sustainability = Business Value

Being energy efficient isn’t just good for the planet. It’s good for your brand.

ESP enables ESG reporting alignment and supports eligibility for carbon credit mechanisms under the UAE’s National Carbon Registry. This matters more than ever, especially when dealing with global clients or partners.

Stay Ahead of Regulations

Green rules are coming. Some are already here. ESP is now directly linked to compliance under Federal Decree-Law No. 11 of 2024, making energy reporting mandatory rather than optional.

ETIP rewards companies that invest in energy-efficient tech and practices. So instead of scrambling to catch up, you’re already compliant—and ahead of the curve.

Made for Big Players

ESP is especially useful for manufacturers, heavy industries, and tech-focused zones.

If your business runs machines, labs, or cooling systems all day—this program was built with you in mind.

The program is aligned with Operation 300Bn, the UAE’s industrial strategy to grow the sector’s contribution to the national GDP. ESP achieves this by lowering the operative costs of manufacturing.

Basically, ETIP is about lowering costs, boosting productivity, and driving cleaner, smarter growth across the UAE’s industrial scene.

ESP and the UAE Corporate Tax Framework

In 2026, ESP participation is no longer just an operational decision—it is a financial strategy. Energy efficiency upgrades now qualify for the UAE’s 50% R&D Tax Credit, introduced in March 2026.

The key requirement? Auditable data. ESP-certified entities generate verified energy performance data through the national MRV system. This data is now accepted as primary evidence for tax credit claims.

This creates a direct link between energy efficiency and corporate tax savings. Businesses that fail to maintain ESP compliance risk losing not just tariff benefits—but also critical tax advantages that protect their margins.

Who Can Apply for ETIP Certification?

Not every business qualifies for ETIP. It’s built for industries that use a lot of power and are ready to prove they’re using it efficiently. Before you start filling out forms, here’s what you need to know:

You Need to Be in the Right Sector

ETIP mainly targets industrial and manufacturing businesses. Think factories, production plants, and tech-heavy operations. This now also includes advanced manufacturing (AI equipment, renewable technologies) and AI-driven data centers, which are among the fastest-growing segments under the 2026 framework. Retail, hospitality, or small offices? Probably not eligible.

High Energy Use Is a Must

Your electricity consumption needs to hit a certain threshold. The idea is to support energy-intensive operations, not light users. Exact numbers can vary by emirate, so check with your local authority.

Watch Out for the Fine Print

Just being in the right sector isn’t enough. You’ll need to meet efficiency benchmarks, submit technical reports, and possibly upgrade outdated systems.

Miss a requirement or fall below mandatory reporting standards, and you risk breaching unmet GHG reporting thresholds—which can disqualify your application or trigger compliance penalties.

Eligibility for Free Zone and Offshore Entities

As of 2026, Free Zone and offshore entities are explicitly covered under the UAE Climate Law framework. Industrial free zones such as KEZAD, KIZAD, and other manufacturing clusters are now required to align with ESP reporting standards.

This expansion is driven by the “Make it in the Emirates” (MIITE) initiative, which now includes over 1,000 locally manufactured products and prioritizes energy-efficient, ESP-aligned entities for incentives, land allocation, and infrastructure access.

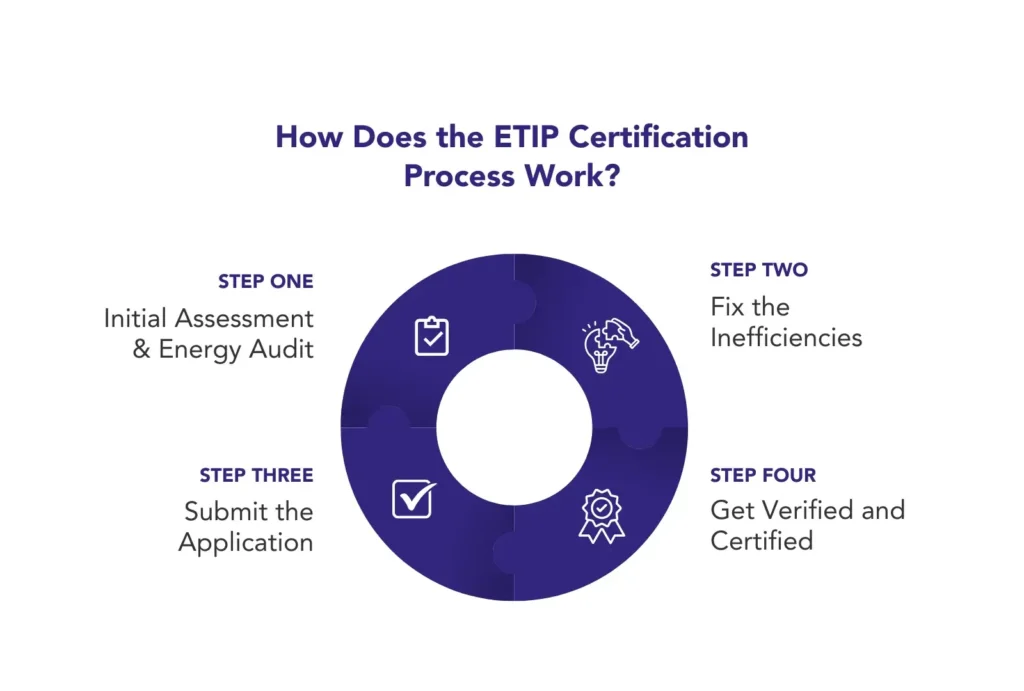

How Does the ETIP Certification Process Work?

Getting ETIP certified isn’t instant. It’s a process—and you’ll need to show your business is serious about saving energy.

Here’s how it works, step by step:

Step 1- Initial Assessment & Energy Audit

Start with a full Comprehensive GHG Baseline Assessment and MRV Registration. This tells you how much energy your facility uses and where it’s being wasted. Most businesses work with approved energy consultants to get this done.

Step 2- Fix the Inefficiencies

Based on the audit, you’ll need to install or upgrade systems to improve efficiency. This could mean better insulation, smart meters, or more efficient machinery. For 2026 compliance, this must include equipment-level monitoring infrastructure, as utility bills alone are no longer sufficient for regulatory reporting. You’re expected to take real, measurable action.

Step 3- Submit the Application

Once you’ve made the upgrades, submit your ETIP application. You’ll need to include technical documents, energy reports, and proof of improvements. All submissions are now routed through the TAMM portal, with UAE PASS required for authentication across all government integrations in 2026. This goes to MoIAT and your local energy department.

Step 4- Get Verified and Certified

Authorities will review your documents and may conduct site inspections. This stage now includes Annual Performance Reporting and Third-Party Verification, ensuring continuous compliance rather than one-time approval. If everything checks out—you’re certified. And that means discounted energy tariffs start kicking in.

Mandatory 2026 Document Checklist

| Requirement | Description | Compliance Logic |

| SLD Diagram | Approved Single Line Diagram of electrical supply | Required to prove connected load > 5MW |

| Direct Debit | Evidence of active direct debit for utility bills | Failure to maintain results in immediate tariff loss |

| Board Reports | 12 monthly board energy reports for re-applicants | Proves governance and executive oversight |

| MRV Data | Data synced to the National MRV system | Mandatory under Federal Decree-Law No. 11 of 2024 |

For 2026, the evaluation is based on a Balanced Scorecard approach: Economic Impact (50%), Productivity (30%), and Energy Efficiency (20%). Facilities with a connected load ≥ 5MW are subject to stricter testing and monitoring requirements compared to smaller sites.

Common Challenges in Achieving ETIP Certification

ETIP can be a game-changer but getting certified isn’t always smooth sailing.

Many businesses miss out simply because they didn’t see the roadblocks coming.

Watch out for these common pitfalls:

Missing or Messy Documents

Authorities want proof. Many applications fail because businesses can’t provide proper reports, data logs, or upgrade records. In 2026, the issue is not just missing documents—it is the inability to maintain real-time, traceable data aligned with MRV system requirements. No audit trail = no compliance.

Confusing Compliance Rules

The technical thresholds for ETIP aren’t always easy to interpret. The biggest challenge in 2026 is separating Scope 1, Scope 2, and Scope 3 emissions, each requiring different reporting standards and verification methods. Many businesses think they qualify until they hit a surprise requirement and stall mid-process. One missed spec can derail the whole thing.

The Global Trade Surcharge Impact

In 2026, global supply chain volatility has introduced additional pressure through import-related costs. High-efficiency machinery, often required for ESP compliance, is now subject to import surcharges of up to 15%, increasing the upfront cost of compliance investments.

Overcoming the Audit Gap: Utility Bills vs. Real-Time Data

One of the biggest gaps businesses face is relying on traditional utility bills instead of real-time monitoring systems. The National MRV system requires continuous data feeds, administrator-level controls, and a minimum 5-year data retention policy. Many firms struggle with system integration and account governance, leading to failed assessments.

Additionally, technical compliance has become stricter. ESMA standards for industrial motors and transformers, effective January 2026, must now be met as part of the certification process. Failure to align with these standards can result in immediate rejection or loss of tariff benefits.

How ADEPTS Supports Your ETIP Journey

Getting ETIP certified doesn’t have to be a headache. ADEPTS acts as your regulatory partner—helping you navigate not just certification, but full compliance under the UAE’s 2026 climate and tax framework. ADEPTS can guide you from start to finish with zero guesswork and no missed steps.

Here’s how we help:

Smart Pre-Assessment Strategy

We start with a readiness check. You’ll know right away if your business has ETIP potential and what needs to change. No time-wasting. No false starts.

This now includes Climate Law Readiness Assessments and Tax Incentive Strategy planning, ensuring your business aligns with MRV requirements while unlocking 2026 R&D tax credits.

Compliance Made Simple

We handle the hard stuff—documentation, reporting, and technical submissions.

You stay focused on your business. We keep everything ETIP-compliant.

Our approach now includes End-to-End MRV and E-Invoicing Integration, ensuring your energy data is audit-ready and aligned with UAE’s digital compliance ecosystem.

Support Even After Certification

Getting certified is just the beginning. ADEPTS helps you maintain compliance so your discounted rates keep flowing, year after year.

We also manage Post-Certification Compliance Audits, ensuring you don’t lose tariff benefits due to reporting failures or system gaps. For failed assessments, ADEPTS provides structured gap reports and remediation strategies to secure re-approval.

Carbon Credit and Registry Support

ADEPTS supports Carbon Credit Strategy development and National Carbon Registry (NRCC) registration, helping businesses convert compliance into measurable financial and ESG value.

With the May 30, 2026 compliance deadline approaching, early preparation is critical. Delays can result in penalties, loss of incentives, and regulatory exposure.

Conclusion

ESP is your operational license in the 2026 green economy. It’s a passport to real savings, stronger sustainability, and long-term growth in the UAE. But in 2026, it is also a shield against regulatory penalties under evolving climate laws.

If you’re planning to launch or scale an industrial business here, this is your chance to get ahead, not play catch-up.

Aligned with the UAE’s Net Zero by 2050 vision and the Circular Economy Policy 2021–2031, ESP is no longer optional—it is central to how businesses operate, report, and grow.

Ready to explore your ETIP potential? Take advantage of the 2026 ESP Admissions Window. Reach out to ADEPTS for a free, no-obligation ETIP pre-assessment consultation. Let’s cut your energy costs and power your business the smart way.

FAQs:

ETIP is for businesses that use a lot of energy. Think factories, manufacturing plants, and tech hubs. If your business runs on heavy machinery or high electricity, this program is for you.

In 2026, this also includes AI-driven data centers, advanced manufacturing, and high-performance computing facilities.

The standard processing time is up to 60 working days through the TAMM portal, but total timelines can still range between 3 to 6 months depending on system upgrades and documentation readiness.

Yes, for reporting; voluntary for incentives. However, failing to report energy data by May 30, 2026, can result in significant fines under Federal Decree-Law No. 11 of 2024.

You will lose your ETIP/ESP benefits in case you fail to comply with the standards. Your discounted tariff will be taken back. You will have to go through a long and complex process if you want to reapply.

Additionally, non-compliance may trigger regulatory penalties and exclusion from future incentive programs.

SMEs can definitely benefit too. This is especially true for small businesses in energy-intensive industries.

With MIITE 2026 targeting 60% SME participation, simplified compliance tracks are now available for smaller entities.

ETIP or ESP certification typically requires renewal every year. Your business must show ongoing compliance with energy benchmarks. This may involve submitting updated energy reports and undergoing periodic reviews to continue receiving the tariff incentives.

This now includes continuous MRV data reporting rather than periodic submissions.

You will need detailed energy audits, technical reports, equipment specs, proof of upgrades, and utility consumption data. Authorities also ask for compliance plans, photos, and in some cases, on-site inspection approvals. Documentation must be thorough and clear.

In 2026, this extends to MRV-integrated datasets, equipment-level monitoring records, and digital compliance logs.

Yes, that is possible. Perhaps not in all cases but in some cases it is possible. There are specific eligibility criteria for these things. Businesses need to check requirements according to that criteria.

In 2026, ESP data is also used to support R&D tax credit claims and carbon credit eligibility.

Inspectors will review your submitted documents and may visit your facility. They’ll check if all upgrades are in place, systems are running efficiently, and reports match real performance. If all is good, you’ll receive or retain your ETIP certification.

This now includes third-party verification and real-time data validation through the national MRV system.

No stress. ADEPTS gives you a clear gap report that shows what went wrong. We guide you through the fixes, help improve your energy systems, and prepare you for a stronger reapplication. This gives you a better shot at getting certified.

We use structured remediation strategies aligned with 2026 compliance standards to help secure re-approval.

ESP stands for Energy support Program. It’s a UAE government plan that gives you cheaper electricity. Only if your business is energy-efficient. It’s built to help power-hungry industries save money while going green. Less waste. Lower bills. Bigger profits.

It is now also a compliance framework linked to national climate and tax systems.

If you run a factory, a manufacturing unit, or a tech-based business. You need to meet certain energy use and efficiency standards. And you must be in an approved sector. If you check those boxes, ETIP could seriously cut your costs.

This now includes Free Zone entities and AI/data center operations under expanded 2026 eligibility.

They look at your energy use, system efficiency, upgrades, and environmental impact. Solid data and a proper energy audit give you a strong chance.

In 2026, this follows a Balanced Scorecard: Economic Impact (50%), Productivity (30%), Energy Efficiency (20%).

Your score depends on energy saved, efficiency ratios, and green practices. Each emirate may score it slightly differently, but the focus is on long-term savings.

Connected load and real-time MRV data now play a critical role in scoring.

Es! ESP covers electricity and gas.

ESP 2.0 explicitly includes both electricity and gas under unified tariff structures.

From audit to approval, the process can take between 3 and 6 months. This depends on how quickly your business can implement efficiency upgrades, complete paperwork, and pass inspections. Delays often happen due to missing documents or unclear data.

However, core approvals are now processed within 60 working days via TAMM.

Yes, the certification must be renewed, usually every year. Your business will need to prove it still meets the energy efficiency criteria. Renewal includes updated reports, performance reviews, and sometimes a follow-up inspection by the authorities.

Ongoing compliance now depends on continuous data reporting rather than periodic checks.

Yes, many free zone entities are eligible, especially those in industrial or manufacturing zones. However, eligibility and tariff discounts can vary by location and utility provider, so it’s best to check with the local energy department for confirmation.

As of 2026, Free Zone participation is formally integrated under national climate mandates.

ETIP applications are reviewed by the Ministry of Industry and Advanced Technology (MoIAT), in partnership with local Departments of Energy and utility companies. These authorities handle compliance checks and make the final decision on approvals.

This now includes coordination with TAQA Distribution and environmental oversight bodies for MRV compliance.

E-invoicing guidelines issued in February 2026 require energy-related transactions to be embedded in metadata for automated compliance and audit tracking.

Yes, particularly for AI data centers, esports facilities, and high-energy server operations, provided they comply with GCGRA standards and energy efficiency benchmarks.

References

- UAE Government. Federal Decree-Law No. (11) of 2024 on the Reduction of Climate Change Effects. Accessed April 15, 2026.

https://uaelegislation.gov.ae/en/legislations/2558 - Ministry of Climate Change and Environment. UAE Climate Law: Compliance Requirements and Obligations for Businesses. Accessed April 2026.

https://bsalaw.com/insight/uae-climate-law-what-every-business-needs-to-know-before-may-2026/ - Ministry of Finance UAE. UAE Electronic Invoicing Guidelines (Version 1.0, February 2026).

https://mof.gov.ae/wp-content/uploads/2026/02/UAE-Electronic-Invoicing-Guidelines_V-1.0-23Feb2026.pdf - Alvarez & Marsal. UAE Electronic Invoicing Guidelines: Regulatory Clarifications and Technical Framework (2026).

https://www.alvarezandmarsal.com/thought-leadership/middle-east-tax-alert-uae-uae-electronic-invoicing-guidelines-february-2026-regulatory-clarifications-and-technical-implementation-framework - Baker McKenzie. United Arab Emirates: Ministry of Finance Electronic Invoicing Guidelines (February 2026).

https://www.bakermckenzie.com/-/media/files/insight/publications/2026/02/united-arab-emirates-mofs-electronic-invoicing-guidelines.pdf - Orchida Tax. UAE E-Invoicing Requirements 2026: Compliance and Penalty Framework.

https://orchidatax.com/uae-einvoicing-requirements-comprehensive-guide-2026/ - RTC Suite. UAE E-Invoicing 2026: Scope, Implementation, and Next Steps.

https://rtcsuite.com/uae-e-invoicing-2026-new-guidelines-scope-and-next-steps/ - NovaSoft. UAE E-Invoicing 2026: Full Compliance Guide and Peppol Framework.

https://novasoft.global/uae-e-invoicing-2026/ - Ministry of Industry and Advanced Technology. Operation 300Bn Strategy Overview. Accessed 2026.

https://moiat.gov.ae/en/strategic-initiatives/operation-300bn - UAE Government Portal. UAE Net Zero 2050 Strategic Initiative.

https://u.ae/en/information-and-services/environment-and-energy/climate-change/net-zero-2050 - OpenPeppol. Peppol Interoperability Framework and E-Invoicing Infrastructure.

https://peppol.org/learn-more/peppol-interoperability-framework/ - Federal Tax Authority UAE. UAE Tax Procedures and Digital Compliance Framework.

https://tax.gov.ae